*Legal disclaimer: The post, the attached Excel model, and all its contents herein are the exclusive property of Continuous Compounding. This post is intended solely for informational purposes and is not to be distributed, reproduced, or transmitted, in whole or in part, for commercial purposes or sale without prior written consent from Continuous Compounding. Any unauthorized use, dissemination, or sale of this research is strictly prohibited and may be subject to legal action. Continuous Compounding assumes no responsibility or liability for any errors, inaccuracies, or omissions in this post or for any actions taken based on its contents. Recipients of this research are advised to conduct their own independent analysis and seek professional financial advice before making any investment decisions.

This post is a revision of my initial post:

GAN Part 4A: Decision Tree Analysis

It was brought to my attention by a follower that there is risk in GAN’s Chilean operations. This is a variable I did not capture in my previous post. In this post, I will evaluate the merger agreement and Chilean operations; and adjust my decision tree analysis to arrive at a new price target for GAN.

Chile Risk:

In the merger agreement, in “Section 8.2 Additional Parent and Merger Sub Conditions,” it states:

“The obligations of Parent and Merger Sub to consummate the Transactions, including the Merger, will be further subject to the satisfaction or, to the extent permitted by Applicable Law, waiver at or prior to the Closing of each of the following conditions (any of which may be waived exclusively by Parent and Merger Sub):

……

(h) Chilean Operations. The National Congress of Chile has not enacted any Applicable Law or issued any Order that has the effect of making the Company’s operation of online gaming illegal in Chile and is not reasonably capable of being overturned, cured or otherwise remedied on or before the End Date.”

*The “may be waived exclusively by Parent and Merger Sub” will be an important detail we will touch upon later in this post. For now, keep a mental note.

Timeline of Online Gambling Regulation in Chile:

On March 7th 2022, legislation for online gambling was filed in Chile’s Chamber of Deputies.

At that point, online gambling was not yet regulated. “The only forms of legal online gambling in Chile are limited lottery games and sports betting offered by two national lotteries.”

The incentive to regulate the industry seems to be to generate tax dollars, as the legislation requires licensees and players to pay the following: “licensees would be subject to an annual fee of approximately US$70,000 and be taxed at a headline rate of 20 percent of gross online gambling revenue, plus an additional 2 percent to be paid to Chilean sports and a mandatory 1 percent return to approved responsible gaming initiatives. Players would also have to pay a monthly 15 percent winnings tax.”

“The regulator would be able to enforce the law by seeking court orders to block unlicensed websites as well as related financial transactions, while only licensed operators would be able to advertise or sponsor sporting events in Chile.”

Due to the lack of regulation, land-based operators were at odds with offshore operators:

“In Chile, online betting is completely prohibited and outside the regulatory framework, and they are illegal and unfair competition,” Mariana Soto, [the president of the Chilean Association of Gaming Casinos], told La Tercera.”

It should be noted that the above is Mariana’s interpretation of the law and is not a factual statement.

The stance by online offshore operators is that because it is not regulated and not prohibited, it is not illegal. Essentially, how can I be charged for breaking a rule that doesn’t exist?

“The Public Ministry firmly rejected these arguments, arguing that there are pending proceedings and that “the non-existence of crime cannot be forced” as a precedent or as a future argument.”

A bill is currently under discussion.

“The bill will ban any online platforms which have been present in the market over the previous twelve months.”

“According to article 13 of the bill: “The Superintendency will reject applications for an operating license when any of the following circumstances occur: having operated a betting platform without the proper operating license, or without the certification that authorizes it to operate in accordance with this law, or advertised or offered its services in Chile in the last 12 months prior to the request.”

In terms of advertisements, operators cannot sponsor “people, entities and/or events that take place in the national territory.”

GAN does not have an operating license and has advertised and offered its services in Chile in the last 12 months.

Coolbet (GAN’s B2C business) became the partner of the Colo-Colo Chilean football team; hence, it has advertised its services in Chile.

“Online operators will not be allowed to offer their services if they have allowed the crediting of user accounts or the payment of bets in Chile and if they have advertised or promoted their services locally.”

Essentially, Coolbet satisfies most, if not all, of the criteria for being rejected an operating license.

In summary, if Coolbet cannot be granted an operating license, then operating in Chile becomes illegal. If the bill is passed, then condition (h) of Section 8.2 of the merger agreement will be hard to satisfy. The only way I see condition (h) being satisfied is if the company has confidence in its ability to cure or remedy the situation. I see a low chance of the ruling being overturned once passed, given how specific and targeted the bill was in specifying conditions for which an application would be rejected. Essentially, any existing offshore operator that is operating in Chile at the moment would be rejected.

Since they are offering operating licenses, I find it strange that they don’t release a clause saying that if the illegal operators pay their fair share of back taxes and fines, they can then be considered for a license. Clearly, the off-shore operators are sponsoring local sports teams and spending marketing dollars to build a player base. Outright disqualifying current offshore operators and inviting new offshore operators seems like a missed opportunity to generate larger sums of taxes on day 1. I believe, from a tax-dollar generation perspective, they should offer a settlement.

Based on the most recent Q3 2023 10Q by GAN, the following is a summary of the stance the company is taking:

In June 2020, Chile required foreign digital service providers, like Coolbet, to register for value-added tax (VAT). VAT is a type of tax added to the value of goods or services at each stage of production or distribution. In September 20th, 2021; Coolbet sought clarification from the Chilean Internal Revenue Service (SII) about how to apply VAT to its services.

In December 2021, the tax authorities clarified that fees paid by users for entertainment services on online gaming and betting platforms, including Coolbet, are subject to a 19% VAT in Chile. This tax is applied specifically to the gross customer deposits on the platform.

On May 13, 2022, the tax authorities stated that unregistered foreign digital service providers would face a 19% withholding tax on payments made through credit cards, debit cards, and other payment methods. This withholding was to be enforced on August 1, 2022. The tax authorities issued a list of noncompliant foreign digital service providers to enforce this withholding. Coolbet was not on this list despite not complying.

As of September 30, 2023, Coolbet has not registered for the Chilean VAT, but it hasn't been listed for withholding either. The company has not received formal notification of any VAT liability.

In March 2023, the tax authorities (SII) stated that they cannot register taxpayers for the simplified VAT regime if their activities have been declared illegal by other state authorities. The Superintendency of Gambling Casinos informed the tax authorities that offering games of chance without proper authorization is illegal in Chile. This led to the exclusion of certain taxpayers (including Coolbet) from the simplified VAT regime.

On September 12, 2023, the Supreme Court of Chile ruled that a local internet service provider and a state-owned land-based casino could block 23 iGaming websites. This ruling was specific to the parties involved and did not establish a legal precedent. Coolbet modified its website URLs in response to this ruling and continued operations.

Coolbet maintains that its activities in Chile are not illegal, based on external legal opinions. The company disagrees with the application of VAT on gross customer deposits and believes that only the fees directly charged by its platform should be taxable. However, due to being excluded from the digital VAT registration, Coolbet no longer considers a VAT liability probable as of December 31, 2022. There is uncertainty about the regulatory environment, potential financial obligations, and the ability to operate in Chile until the tax authorities resolve their position. This uncertainty could lead to fines, penalties, additional expenses, or even exiting the market. Revenues from Chile account for a significant portion of Coolbet's overall revenue.

My analysis of the situation in Chile:

*I am not a lawyer. Please seek guidance from a professional lawyer.

My interpretation of the events is as such. Chile lacks regulation for iGaming and online sports betting. Due to this lack of regulation, operating an online gambling website isn’t prohibited, so it is not illegal. This is similar to when I was in elementary school, when the teacher posted certain rules of conduct that should not be violated. What if there is something you shouldn’t do, but it isn’t written down as a rule?

Now it is normal for gambling websites to be charged VAT taxes on the earnings of online operators, but definitely not on gross customer deposits. This part I completely agree with GAN on. Being taxed on gross customer deposits of 19% would be a completely unreasonable interpretation and not a reasonable application of the law. One thing I did learn in my undergrad law course is that if a non-compete clause in an employment contract is more than 2 years, then it is not enforceable. So if a customer deposits $100, the business has to pay the tax authorities $19. If the customer deposits $100 and withdraws $100, the casino is out $19. No casino business on earth would be profitable under such a ruling. The house edge would have to be crazy for the online casino to be profitable. In a sense, SII potentially fumbled the ball here by creating a rule that is next to impossible to follow if enforced.

GAN sees this as an unreasonable application of the law, so it refuses to pay.

SII cannot register GAN for the VAT regime, given that they are declared illegal by other state authorities. Because they can’t be registered, they cannot pay taxes, even if they wanted to. Furthermore, they were not on the “noncompliant list of unregistered foreign digital service providers” that was issued on December 28, 2022. I have no clue why Coolbet is not on this list. This could simply be another fumble by SII. If my instincts are correct, if the Chilean tax authorities come after Coolbet for back-taxes dating before Dec 28th, 2022; Coolbet will question the tax authorities on why they were not on their non-compliant list.

Even if Coolbet is able to defend their tax liability from before Dec 2022, they may still be on the hook for back taxes post-December 2022.

Coolbet was on the list of 23 iGaming websites that needed to be blocked by Chile’s internet provider. This is something they avoided mentioning in their 10Q with fancy lawyer speak. “In response to the ruling, the company modified the URL and resumed operations.” I believe the time is ticking on when they will be forced to exit the Chile market. Coolbet simply saw a grey area in the ruling and avoided exiting Chile by simply changing the URL. If future rulings are more precise, then it’s only a matter of time before Coolbet runs out of grey areas to take advantage of.

I believe GAN’s Chilean operations face significant headwinds in the near term.

(h) Chilean Operations. The National Congress of Chile has not enacted any Applicable Law or issued any Order that has the effect of making the Company’s operation of online gaming illegal in Chile and is not reasonably capable of being overturned, cured or otherwise remedied on or before the End Date.”

I see 2 paths forward:

Path 1 (favorable): GAN’s operations are not illegal. Once new iGaming regulations are put in place, then it would be illegal if GAN continues to operate in Chile. They need to register for a license if they want to legally operate. Since GAN cannot qualify for an operating license, GAN will not be able to legally operate once full regulation is put in place. GAN can still sell their company to Sega Sammy, given that their operations in Chile are not illegal. Condition (h) says nothing about GAN having to continue operations in Chile.

Path 2 (unfavorable): The National Congress of Chile has deemed GAN’s operations illegal during the period prior to full regulation. GAN cannot fulfill condition (h), hence cannot sell to Sega Sammy or renegotiate. I expect GAN to lawyer up and attempt to overturn this decision if it were to happen.

The puzzling part is that all this news came to light prior to Sega Sammy’s acquisition offer. Both Sega Sammy and GAN hired independent investment firms to perform due diligence; it should have been unlikely for them to miss this.

My thoughts are that Sega Sammy simply does not want legal trouble from acquiring GAN. The independent investment team Sega Sammy hired should have gone over GAN’s Chile operations and should have been able to determine that GAN’s days in Chile are numbered. I believe their current offer should heavily discount the value of GAN’s Chilean operations. I wouldn’t be surprised if 0 dollars were allocated to the value of Chilean operations, given the potential for fines, fees, and lawyer fees.

If my above assumption is true, I believe condition (h) is put in place simply as an option to avoid a huge headache if the Chile situation gets too complex, so Sega Sammy can just walk away, but if the Chile situation is simply back-taxes, for example, then Sega can waive condition (h) or terminate the existing merger agreement and renegotiate a lower bid given the additional leverage they have on their side.

“The obligations of Parent and Merger Sub to consummate the Transactions, including the Merger, will be further subject to the satisfaction or, to the extent permitted by Applicable Law, waiver at or prior to the Closing of each of the following conditions (any of which may be waived exclusively by Parent and Merger Sub):”

My interpretation of the events is that if the Chilean operations are deemed illegal, the value of B2C in Chile is worthless (possibly negative if GAN gets taxed and fined). Thus, Sega Sammy would simply come back with a lower offer if the current offer doesn’t already heavily discount Chilean operations. Sega Sammy’s intentions are to enter the iGaming market in the US; that is where the big bucks are, so if GAN can no longer operate in Chile, then they can just pay less.

Other Facts About the Merger Agreement:

There is also a “Go Shop” provision that allows a new bidder to come into the picture. If the company does attain a higher offer, they will have to terminate the merger agreement with Sega Sammy. If this were to happen, GAN would have to pay a termination fee of $6,000,000. This amounts to roughly $0.13 per share. Hence, if a new bidder were to come into the picture, they would need to offer at least $2.10 to match Sega Sammy.

Termination fee: $6,000,000

Decision Tree Analysis:

Updated decision tree analysis, sensitivity analysis and an updated Excel model will be released to Free Subs 1 week after Paid Subs. Consider a free trial, referring a friend, or treating me to a cup of coffee this month to gain instant access!

Click the below Google Drive link to access the Excel model and to play around with the assumptions:

Let me explain what assumptions you see in the above table:

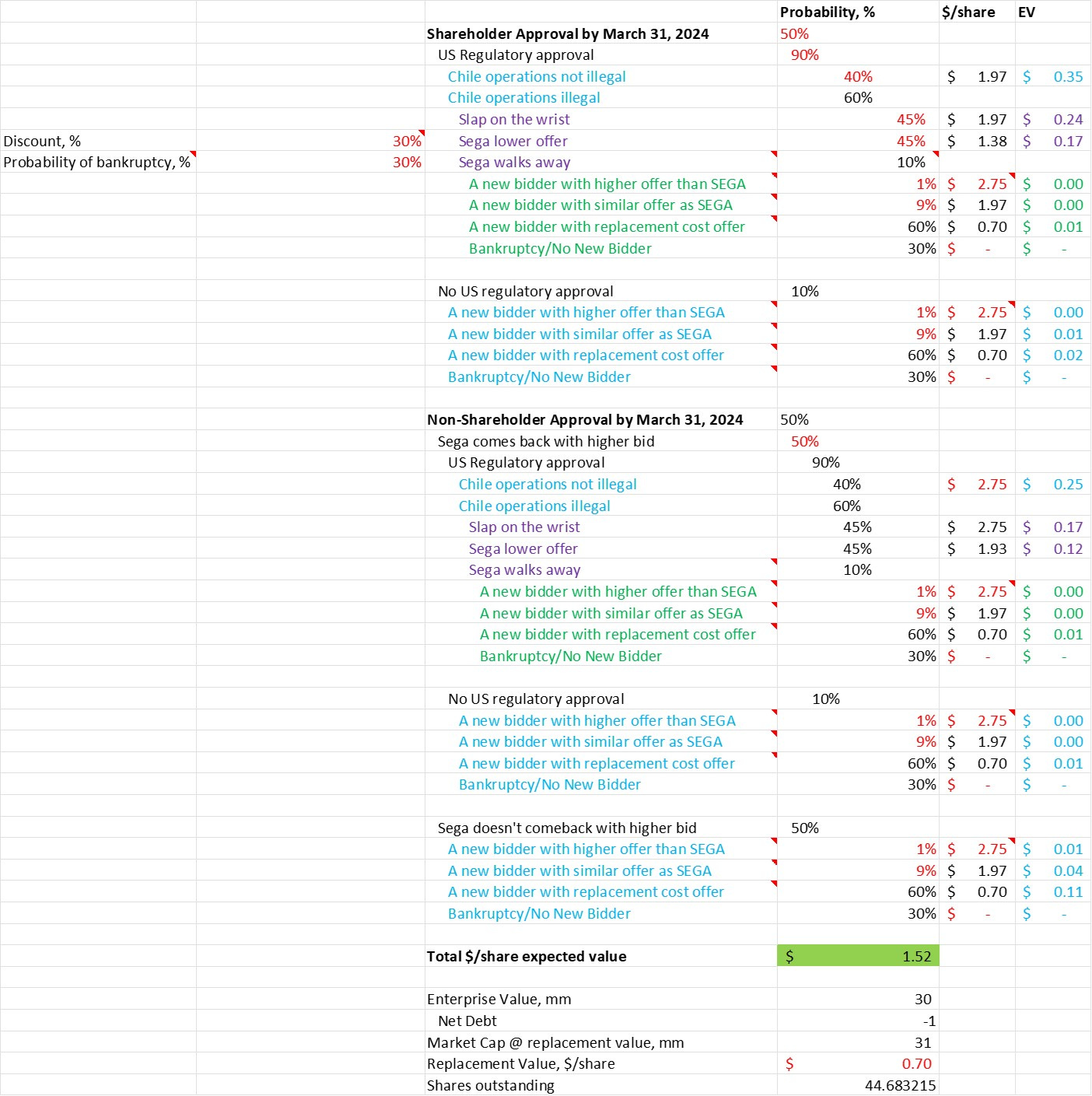

Shareholder approval by March 31st, 2024:

There is an assumed 50% chance of shareholder approval by March 31st, 2024

Following approval, there is a 90% chance SEGA’s takeover of GAN will be approved by US regulators

Even if we are approved, we must fulfill condition (h) in the merger agreement. It is assumed that there is a 40% chance Coolbet’s Chile operations are deemed not illegal.

If Chile operations are deemed illegal (60% chance), there is a 45% chance SEGA can turn a blind eye if we are subject to minor fines, 45% Sega comes back with a lower offer (30% discount) if the initial $1.97/share offer didn’t already discount Chilean operations, and 10% that Sega walks away

If SEGA walks away, then:

There is a 1% chance there is a higher offer

9% chance of a similar offer

60% chance of a replacement cost offer at $0.70

30% chance of going bankrupt.

If not regulatorily approved in the US:

There is a 1% chance there is a higher offer

9% chance of a similar offer

60% chance of a replacement cost offer at $0.70

30% chance of going bankrupt.

Non-shareholder approval by March 31st, 2024:

There is a 50% chance of non-shareholder approval by March 31st, 2024

Given non-shareholder approval, it is assumed that, with a 50% probability, Sega will come back with a higher offer price.

Again, probability of regulatory approval is assumed to be the same in the shareholder approval and non-approval scenarios.

I believe if Sega were to raise their offer, they could raise it to $2.50–$3.00. There is nothing academically rigorous about this estimate. The logical step-up from 90mm EV is to $110-130mm EV or $2.50 - $3.00/share range.

Chilean Operation risk is exactly the same as in the “Shareholder Approval” scenario, except we start off with a $2.75/share offer price given the higher bid.

If there is no US regulatory approval or SEGA refuses to raise their bid and walks away, then:

There is a 1% chance there is a higher offer

9% chance of a similar offer

60% chance of a replacement cost offer at $0.70

30% chance of going bankrupt.

*Replacement cost of $0.70/share or EV of 30mm

On Nov 24th, 2023; GAN ended the trading day at $1.51/share. Based on the above assumptions, I arrived at $1.52/share.

*By tweaking all the “a new bidder with higher offer than SEGA” from 1% to 0%, we arrive at $1.51/share.

Sensitivity Analysis:

Here is a sensitivity analysis of changes in “Shareholder Approval Rate %” and “Chilean Operations Not Illegal %”

Let’s see what set of assumptions allows us to arrive at the $1.51 price at the Nov. 24th close price.

Based on the above sensitivity analysis, we arrive at $1.51 roughly if shareholder approval drops to 30% in March 2024, and there is a 50% chance that Chilean operations are deemed not illegal.

If shareholder approval increases to 60% in March 2024, but the probability of “Chilean Operations Not Illegal %” drops to 30%, then we arrive at $1.51 as well.

I will allow you to view the table for the other variations.

Regulatory Approval Analysis:

I already conducted a regulatory approval analysis in my original post. You can review my US regulatory approval analysis here:

GAN Part 4A: Decision Tree Analysis

It shows the market agrees with my original analysis that US regulators are likely to approve the merger. This made me bullish for the wrong reasons, as I was not factoring in Chilean operation risk. I believe that given where the market price stands today, the only way for the price to make sense is a very high US regulatory approval rate (90%+). If the US regulatory approval rate drops meaningfully down the road, then the current market price will drop substantially.

Shareholder Approval %

I have nothing new to add from my previous post

Summary:

Hence, one should purchase shares of GAN at $1.51 primarily if:

The probability of Chilean operations being deemed not illegal is greater than 40%

If the probability of shareholder approval is greater than 50%

One believes regulatory approval will be higher than 90%

If you believe Sega will come back with a higher bid that is equal to or greater than $2.75 per share

My course of action:

It is important to understand one’s circle of competence. Here are my major disadvantages in assessing this situation:

For one, I am not a lawyer. My knowledge of the law stems from 1 undergraduate course.

I am not a merger arb. specialist, so I don’t have a plethora of former experience to draw upon. Although I do hope to improve in the long run,

The news sources I read in English about Chile's online gambling regulations are secondary sources. This puts me at a disadvantage because someone who knows Spanish would be able to read primary sources and generate a more accurate interpretation of facts. I am interpreting the interpretation of someone else.

In investing, you need to stay in the game; this investment has the potential to drop to its replacement value or 0 in bankruptcy, hence risking substantial capital loss. You should also compare this opportunity to other opportunities offered to you on the market. At the moment, Jeremy Raper has started an activist campaign on Bragg Gaming (BRAG/BRAG.TO). This opportunity offers high upside with limited downside. I would much rather focus my energy on BRAG than GAN atm.

You may read my analysis of the BRAG activist situation here:

Jeremy Raper Goes Activist on BRAG

In summary, GAN seems fairly valued, with many what-ifs and a large downside potential. Combining the potentially fair valuation with my list of disadvantages, I would rather sit on the sidelines until more of the story unfolds and the odds get significantly better in my favour. You don’t need to swing at every opportunity that comes at you.

Disclosure: I currently hold no position in GAN, Gan Ltd.

Review former posts:

GAN Part 1: A Quick Overview of GAN Pre-Acquisition

GAN Part 2: Post-Acquisition Offer Analysis

GAN Part 3: SEGA SAMMY PRICE DROP TODAY (Quick Pitch/Update)

GAN Part 4B: Decision Tree Analysis (Factoring Chilean Operation Risk)

*You should read Part 4B before Part 4A. Part 4A was my original decision tree analysis, but I have since factored in Chilean Operation Risk.

GAN Part 4A: Decision Tree Analysis

Thanks for your support!

To stay up-to-date or receive notification of when I release my latest stock pitch, please follow:

Twitter: https://twitter.com/compoundersEX

Instagram: https://www.instagram.com/compounders.ex/

YouTube: https://www.youtube.com/@continuouscompounding

Want to enjoy paid memberships for free? Help me grow by referring a friend!

1. Share Alan’s Substack: Continuous Compounding.

When you use the referral link below or the “Share” button on any post, you'll get credit for any new subscribers. Simply send the link in a text, email, or share it on social media with friends.

2. Earn benefits. When more friends use your referral link to subscribe (free or paid), you’ll receive special benefits.

Get a 1 month comp for 1 referrals

Get a 3 month comp for 5 referrals

Get a 6 month comp for 10 referrals