Unveiling My Highest Conviction Stock!

Oricon (TSE-4800)

*Legal Disclaimer: This post and all its contents are for informational or educational purposes only. Continuous Compounding assumes no responsibility or liability for any errors, inaccuracies, or omissions in this post, links, attachments, or any actions taken based on its contents. The information sources used are believed to be reliable, but accuracy cannot be guaranteed. Recipients of this research are advised to conduct their own independent analysis and seek professional financial advice before making any investment decisions. The opinions expressed by the publisher in this post are subject to change without notice. From time to time, I may have positions in the securities discussed in this post.

This post and all its contents herein are the exclusive property of Continuous Compounding. This post is intended solely for informational purposes and is not to be distributed, reproduced, or transmitted, in whole or in part, for commercial purposes or sale without prior written consent from Continuous Compounding. Any unauthorized use, dissemination, or sale of this research is strictly prohibited and may be subject to legal action.

Disclaimer: I am long shares of Oricon (TSE-4800) at the time of publishing this post.

The single best Japanese company I’ve ever found is Oricon (TSE-4800).

This was a once-in-a-lifetime find for me, and sadly the company is performing an MBO to buy out the shares at 1332 yen per share.

I am releasing my research to the public because I am hoping shareholders do not tender or we get the acquirer to raise their bid because, although a 60-70% gain is nice, the company has the potential to easily be a 1-7x bagger.

My full deep dive is here: Stock With Hidden License to Tax Everything

After reading my own deep dive, I realize that I was too wordy and didn’t get to the meat of my investment thesis until halfway through. My goal in this post is to get to my core investment thesis asap!

Table of Contents:

Brief Company Overview

Segment Overview

Customer Satisfaction Survey

Customer Referral

Business Economics

Customer Satisfaction Survey

Customer Referral

Upside Potential

Commentary on MBO

What is Oricon?

Oricon used to be known for its music rankings. Due to their recognition as the top music-ranking list in Japan, they ventured into music sales and ringtone sales. Their business model crumbled once Apple released the iPhone because Apple does not allow anyone else to sell music on their iPhone besides iTunes/Apple Music. The business model further died off given music streaming.

Oricon has made a full transition into the following 4 segments:

Customer Satisfaction (CS) Survey Business

News Distribution and PV business

Data Service Business

Advertising Business

The Customer satisfaction survey business is Oricon’s core business, where they conduct customer satisfaction surveys and publish the results into ranking lists. The top 3 winners of any ranking list can pay Oricon to use their Oricon trademark logo. I will go in depth later in this post.

For the News Distribution and PV business, Oricon produces over 3,500 entertainment-related news articles, paid PR feature articles, and videos per month.

This content is distributed to its own channels:

YouTube - 2.34 mm subscribers

Twitter/X - 1.6 mm followers

Facebook - 164k followers

Instagram - 43.7k followers

Line - 3.69 mm friends/followers

The content is also distributed to third-party news distributors, such as Yahoo News and other major websites and apps.

Next is the Data Service Business, where Oricon simply collects sales data for music, videos, and books. Revenue is received from broadcasting stations and e-commerce sites for accessing or using Oricon’s database and ranking data.

Lastly, there is Advertising, which was a recent cheap acquisition in Oct 2024, which gives Oricon the ability to upsell companies in its network advertising services.

Key Highlights:

Good (B) management and excellent (A) business economics at an attractive price (A-)

Oricon is an asset-light business with 30%+ normalized operating margins. The business is growing, and margins can further improve with operating leverage.

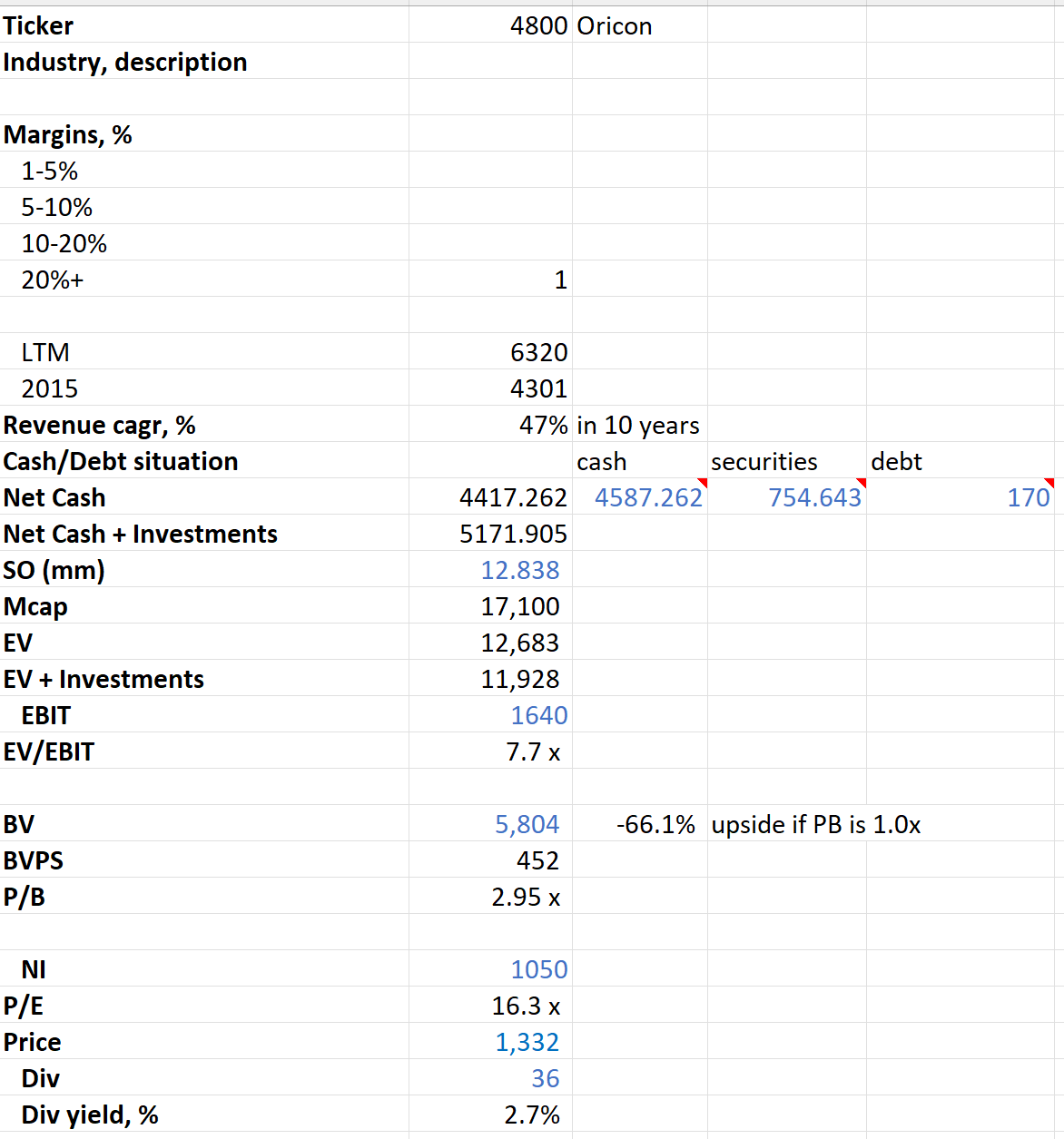

As of Aug 8th, 2025; Oricon trades at:

816 yen per share or 10.5bn MCap.

Lots of cash and very little debt. Net Cash of 3.4 bn yen (180 mm debt, 3.6 bn in cash)

EV = 7.0 bn yen. If including 713 mm yen of investment securities, then EV = 6.4 bn yen.

Valuation Metrics:

4.9x FY2025 (Mar 2026) EV/EBIT excl. LT investments

4.4x FY2025 (Mar 2026) EV/EBIT incl. LT investments

10.9x FY2025 P/E

1.95x Current P/B

1.75x Current P/S

4.4% dividend yield or ¥36 per share

18% FY2025 ROE

Stock is undervalued, as the market is underestimating the company’s ability to grow

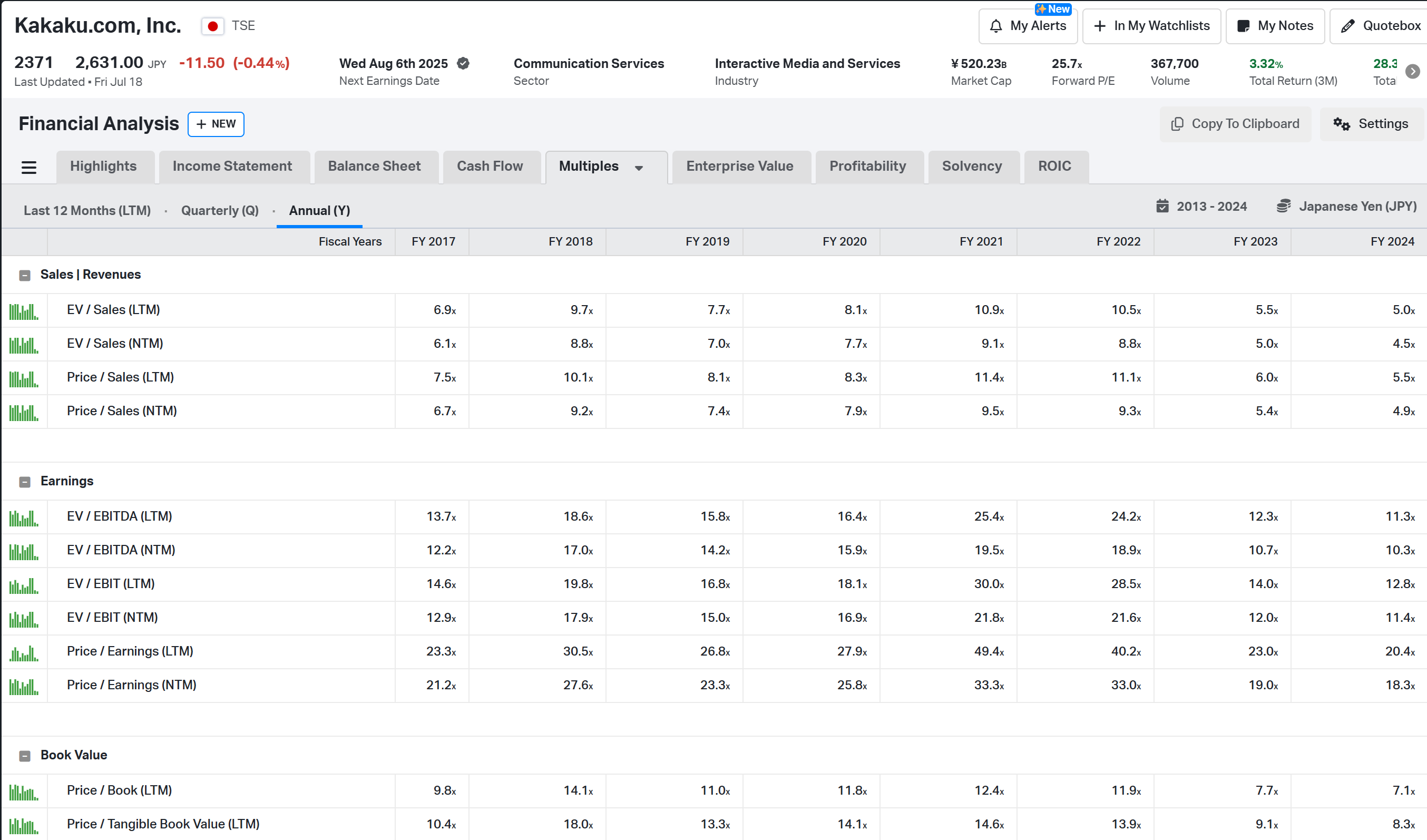

The market does not understand that the stock has a positive flywheel in motion that can lead to multiple expansion at levels similar to Kakaku.com (2371). Kakaku.com’s range of valuation metrics over the last 10 years:

LTM EV/EBIT: 11.4x-21.8x

LTM P/E: 20.4x-49.4x

LTM P/B: 7.1x - 16.6x

LTM P/S: 4.9x-10.1x

If Oricon can become the de facto customer satisfaction ranking list in Japan, the company could generate a 60-200% return in 1-3 years, with an even larger upside, a 2-7x multi-bagger in the best-case scenario. All this upside with very little risk in current valuation, a 4.4% dividend yield, and management’s track record of opportunistically buying back shares.

This is a GARRP investment: Growth at a really reasonable price

Consider Supporting Continuous Compounding!

Paid subs made +50-75% on Oricon!

Paid subs get first dibs on my actionable and timely stock pitches.

This stock pitch was released in Aug 2025. Not bad for a less than 1-year holding period!

For a limited time, you can get 50% off the Annual Subscription ($15 USD/month) → LINK

*Promo ending in 2 weeks.

Here are some sample customer testimonials:

The key role for an analyst in helping the portfolio manager is to increase lift.

Lift is assessed using 3 primary criteria:

hit rate on bets

number of bets

sizing on bets (conviction)

My Substack primarily contributes to factors 1 and 3. I value quality over quantity. I spend a lot of time on names, 100-150 hours for some ideas. The time spent and the quality of the research are what provide readers with conviction. To use a sports betting analogy, I understand the stock so much better than any of the shareholders that I can better assess the true line of a stock. So when there is a massive mispricing and the downside is limited, you can bet big!

Examples of returns:

Oricon - 4800: +70%

Glory - 6457: +80%

AGF.B: +100%

Fast Fitness Japan - 7092: +70%

Furyu - 6238: +25%

SK Japan - 7608: +100%

Round1 - 4680: +100%

Haier - 690D: +75%

My hit rate is above 80% on published ideas. I’ve only had 1 major loss (CNTY, -50%), which was a stock I pitched to start off my Substack in March of 2023. So since April 2023, I haven’t had a position that lost more than 10%, whereas all my winners have generated very meaningful returns, as evidenced above.

My paid sub has very much paid for itself if you blindly and evenly allocated simply $1000 USD to each of my ideas.

Limited Time Offer:

Summer Special Promo! 50% Annual Subscription (15 USD/month) → LINK

Summer Special Promo! 30% Monthly Subscription (21 USD/month) → LINK

*Promo ending in 2 weeks.

Let me first touch upon the superior business economics of their core business, the customer satisfaction survey business.

Communication Business Segment

Customer Satisfaction Surveys

News Distribution/Page Views (PV)

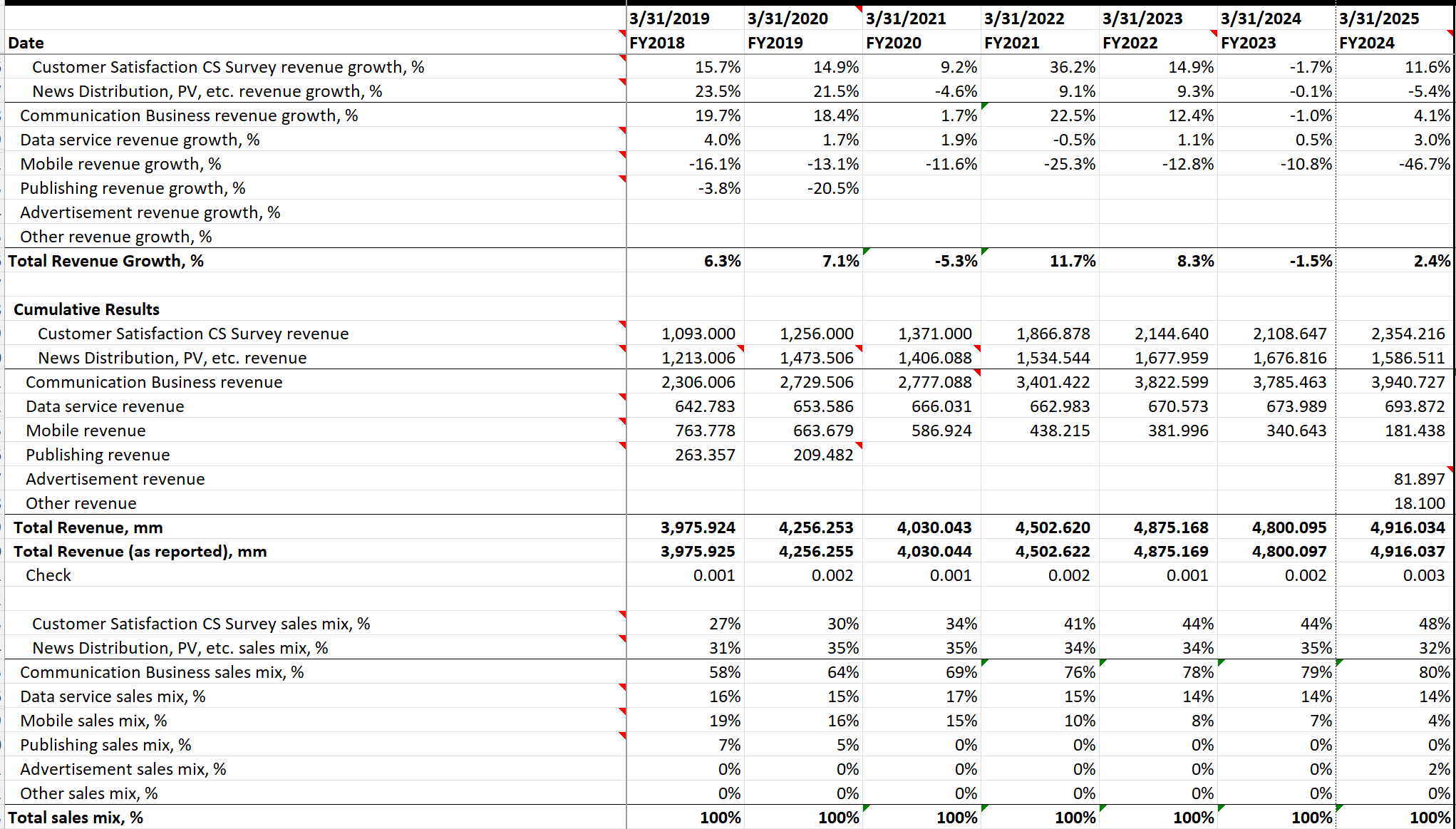

Oricon’s largest segment is the communication business segment, with the customer satisfaction survey and news distribution/PV segments being the company’s core businesses. The segment accounts for 80% of revenues. So let’s dive into the customer satisfaction survey segment first:

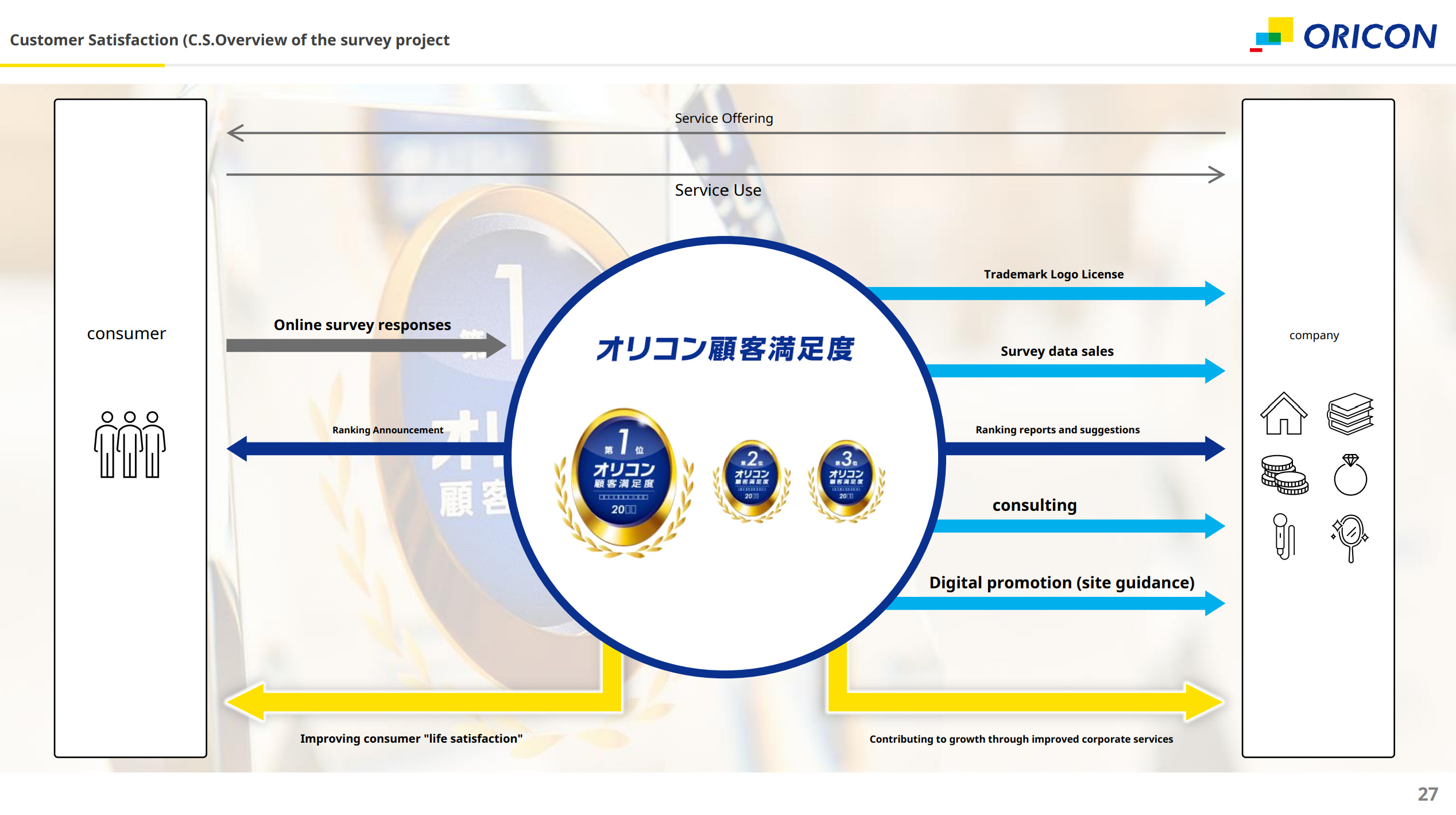

Customer Satisfaction (CS) Survey Business:

CS Segment Overview:

The customer satisfaction survey business is Oricon’s cash cow and the most important segment Oricon operates in.

Within the CS segment there are 4 revenue segments:

Trademark usage

Customer Referral

Data Distribution

Other (Consulting)

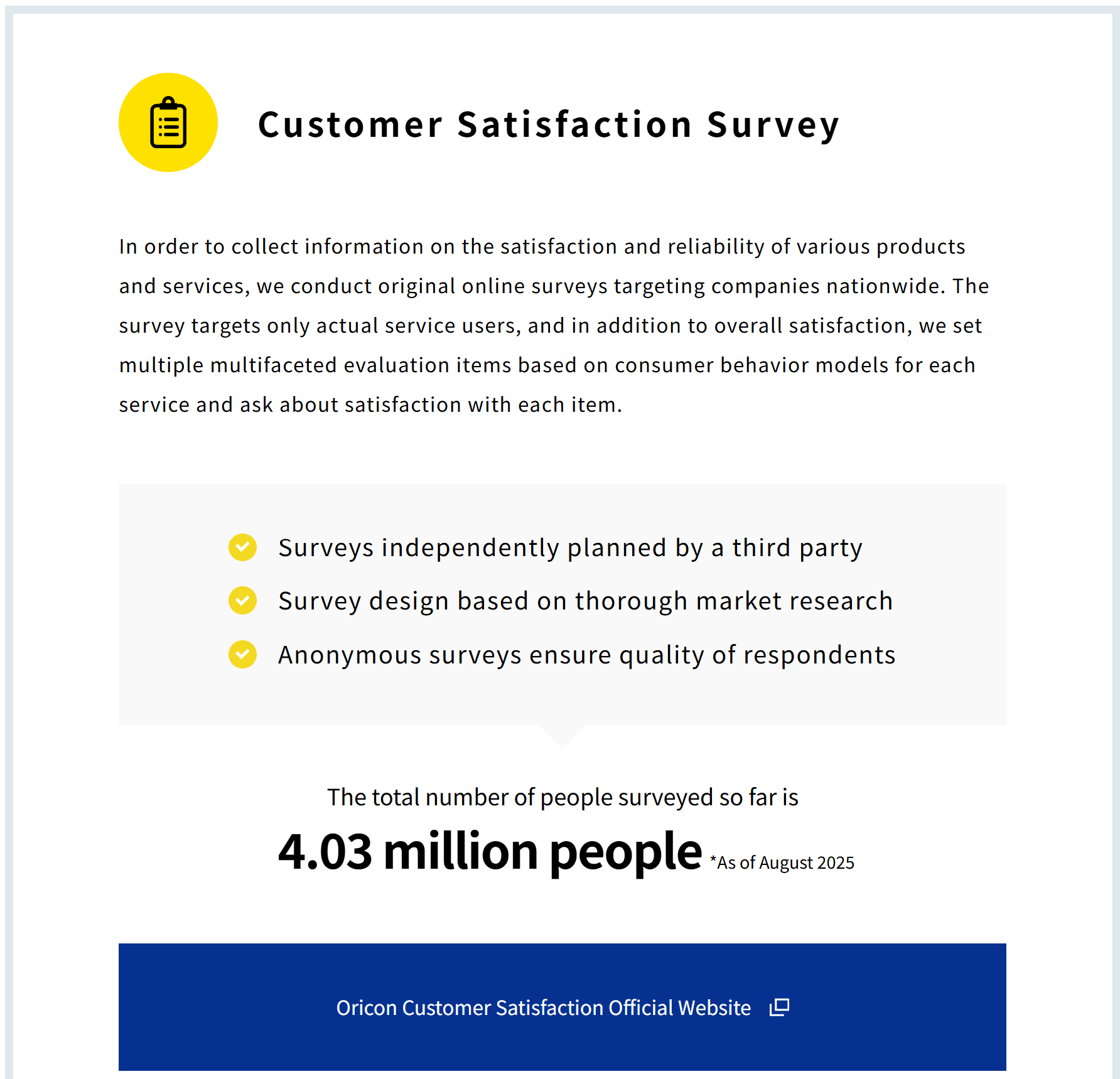

Oricon conducts online customer satisfaction surveys of users of various services. Customer satisfaction is ranked in an independent, fair, and neutral manner. (See the appendix at the bottom to learn more about the Oricon customer satisfaction survey process).3

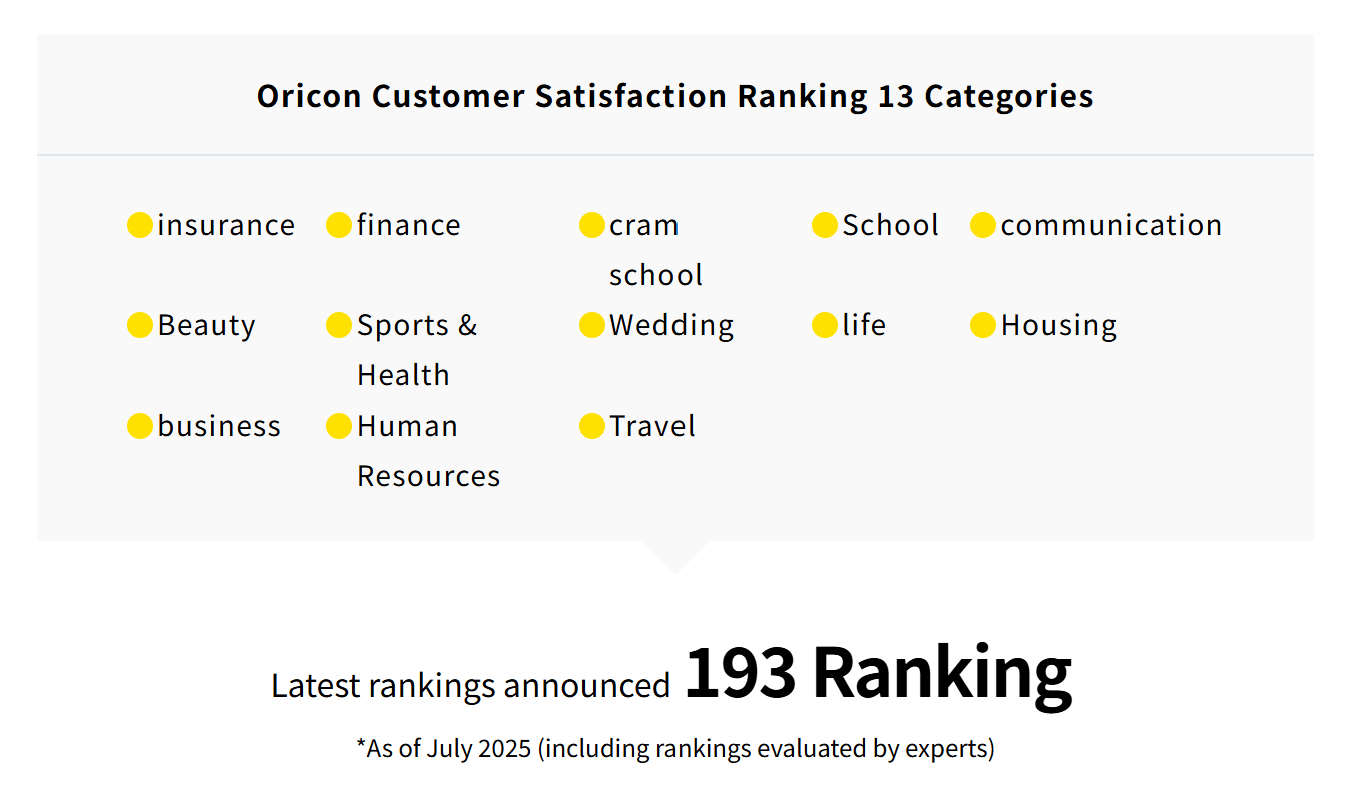

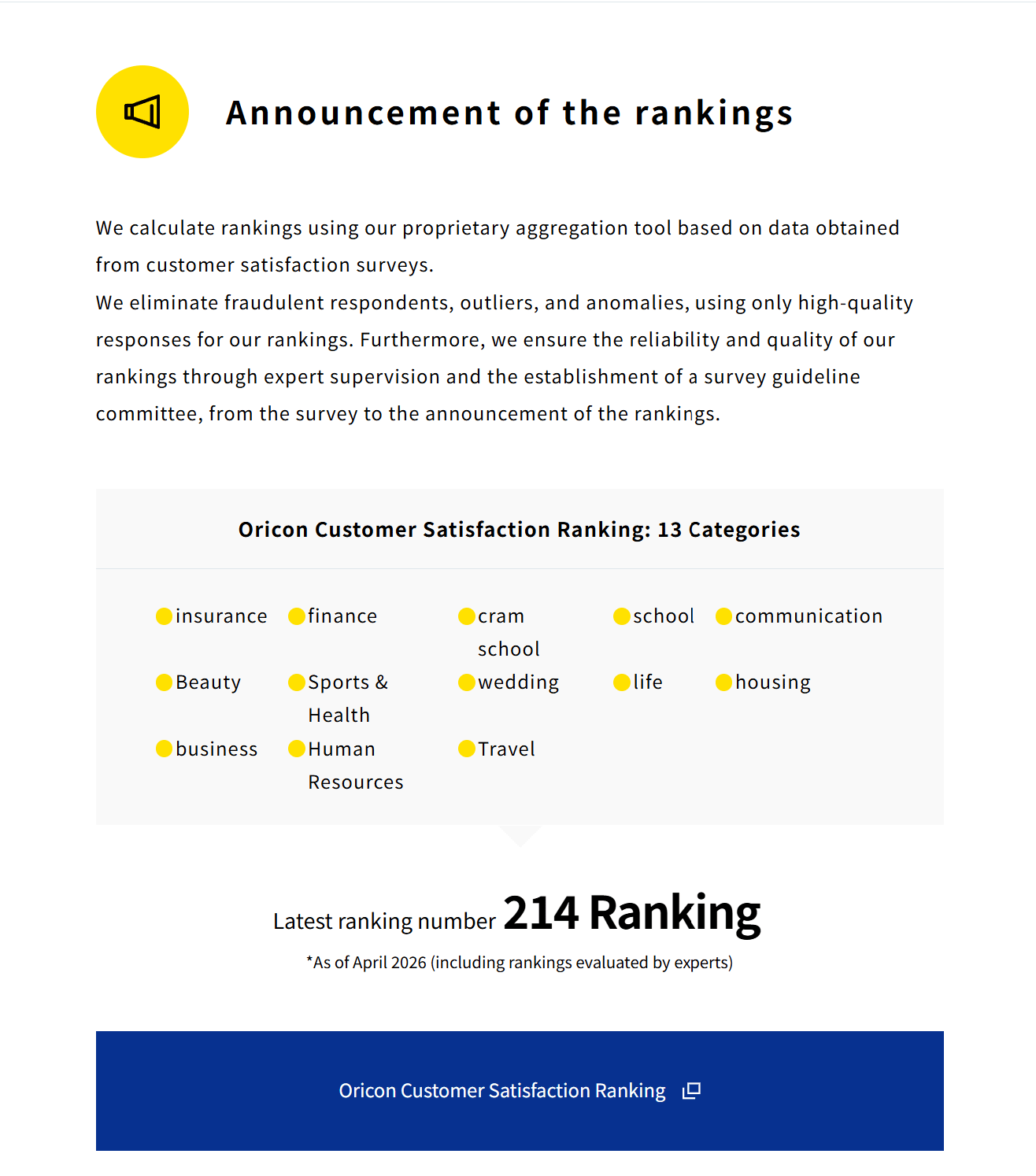

Oricon currently has 193 rankings, as of July and August 2025, spanning 13 categories:

From the surveys, Oricon gives awards to the top 3 winners of each ranking list.

Trademark Usage:

Companies that want to utilize their ranking in ads need to sign a contract and pay a fee to license Oricon’s unique trademark logo. The contract allows the company to use the trademark for 1 year.

Just to clarify, Oricon is getting paid to distribute a JPEG!

1st to 3rd place Oricon Trademark Logos Below:

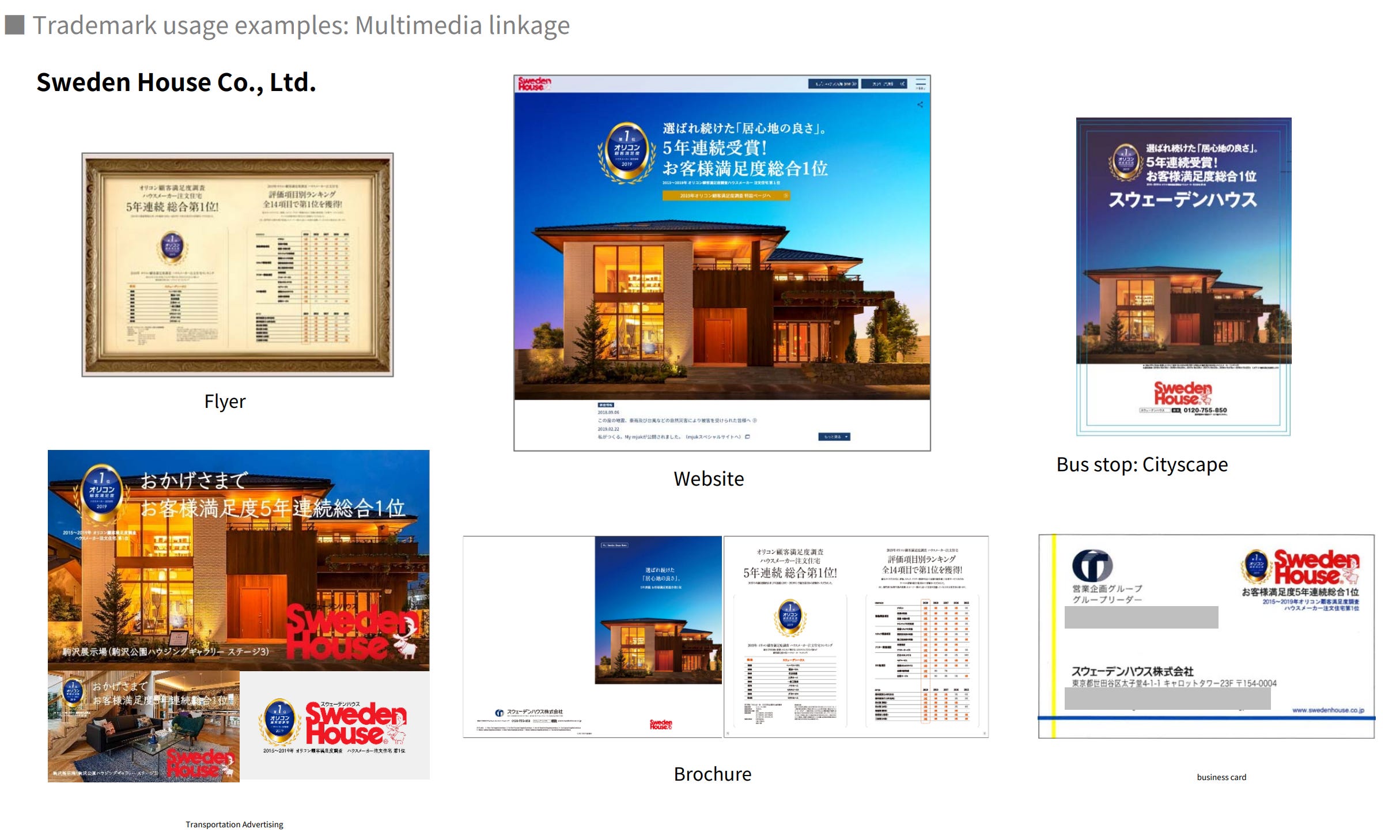

Examples of how trademark logos are showcased:

Infographic of Customer Satisfaction Survey Business Model:

Live footage of me stumbling upon an Oricon trademark logo when I was looking into Oricon’s comps. Kakaku (2371) has a website called “Job Box,” which is an HR website for people looking for jobs. When I was looking into Job Box, an Oricon trademark logo showed up, mentioning how Job Box is No. 1 in job information services. Talk about coincidence!

In the customer satisfaction survey segment, trademark revenues make up over 70% of revenues.

Digital Promotion (Customer Referral) Segment

Oricon’s rankings are published on its ranking website, where the public can see the companies considered in the survey, the survey questions asked, and the survey results.

In order for a company to directly link their company website to Oricon’s ranking list, they must enter into a customer referral contract, paying Oricon based on the number of customer referrals directed to their company page; hence, the higher the traffic to Oricon’s ranking page, the better.

My interpretation of this is that the companies who sign up are paying a variable fee for this service, so it is different than the trademark segment in that there likely is little to no upfront fee.

The interesting part of this segment is that if there are 10 companies in the survey, linking one’s website is not limited to just the top 3 award winners. All companies can pay to refer customers to their website.

Keep this at the back of your mind. The business economics of this part are insane, and I will come back to it later in this pitch. For the time being, remember the following 4 things:

To have a clickable link, companies have to enter into a customer referral contract where they pay per click

The higher the traffic on Oricon’s page, the more Oricon makes from customer referrals

The more ranking lists and the more trademark logos get used in ads from winning customers, the more exposure Oricon gets, and hence, the more traffic gets driven to Oricon’s ranking list website.

All companies on the ranking list can sign a customer referral contract

Data Distribution:

This segment is simply the sale of survey data and additional insights.

Other (Consulting):

Oricon offers consulting services where companies can hire Oricon to conduct research on their own company and its stakeholders to extrapolate insights that can help improve customer satisfaction.

Limited Time Offer:

Summer Special Promo! 50% Annual Subscription (15 USD/month) → LINK

Summer Special Promo! 30% Monthly Subscription (21 USD/month) → LINK

*Promo ending in 2 weeks.

Business Economics and Revenue Growth Analysis:

Customer Satisfaction (CS) Survey Business:

In the customer satisfaction survey segment, trademark revenues make up over 70% of revenues.

Trademark Business Economics:

The core of my investment thesis rests on Oricon’s ability to turn the trademark usage into the consumer gold standard for customer satisfaction rankings.

Oricon’s trademark is, in ways, a positive self-reinforcing flywheel. Large companies like Sony Insurance will use Oricon’s rankings in their advertisements.

Those familiar with Oricon music rankings will recognize Oricon. Those curious about Oricon’s credibility in rankings outside of music may think to themselves,

”Well, if Sony is using their trademark in their advertisement, surely they must be legitimate.”

By association, this pairing of large brands with Oricon’s trademark logo reinforces trust in the eyes of the consumer.

In the social media age, we live in a world driven by impressions. When Sony puts out an ad, how many impressions do you think that generates?

Sony’s ad that generates thousands, if not millions, of views has Oricon’s trademark logo on it.

An individual unaware of Oricon’s non-music-related rankings may perform due diligence on Oricon’s trademark logo and realize it’s Oricon from the Oricon music rankings. This may bring up nostalgic childhood memories and reinforce trust in the Oricon trademark.

This is simply 1 trademark logo on 1 ad from 1 company. Oricon has 193 rankings, with the top 3 being privy to the trademark logo. Creating potential ad opportunities from 379 companies. Depending on the company’s reach and ad spend, the number of impressions may vary, but the key takeaway here is that companies are paying Oricon to spread Oricon’s trademark logo—Oricon is receiving free marketing and organic exposure.

This free exposure leads to curious consumers heading over to the Oricon ranking website. Oricon charges companies a customer referral fee based on the number of clicks to link their company’s website on the ranking list directly. If they don’t pay the customer referral fee, customers will have to Google search the company, which runs the risk of poor SEO rankings and other competitors having a higher ranking due to sponsored ads.

This next part is very important to understand. Reread it a few times if you have to:

So you are telling me I have to pay Oricon to use their trademark. A customer sees my ad and is curious about the award I won. The customer goes to the Oricon ranking site to see the ranking list. While the customer is on the ranking list, if the customer wants to click a convenient link to see my company website, I have to pay Oricon as well? Did I just pay to direct traffic to the link that I paid for as well?

I hope you get the humour in this and how great the business economics are for this to happen. The more “Sony Car Insurance” spends on ads, the more money Oricon generates from their customer referral arrangement.

Referring to Oricon’s ranking lists can be habit-forming. There will come a point where customers who have previously relied on the rankings will visit the rankings on their own. This would be the next stage of growth and credibility I hope Oricon can attain.

In an interview, if an interviewer asks you about your former team at your previous firm, the optimal answer is to only give compliments, such as “hardworking,” “productive,” and “collaborative.” The interviewer will subconsciously associate all those nice qualities with you as well.

What do you think happens to the consumer’s subconscious when the No. 1 car insurance, real estate brokerage, job search, or telecommunication company uses Oricon’s trademark logo in its advertising? Gradually consumers will subconsciously associate Oricon with great companies.

If the assumption is that Oricon is still developing its reputation, then by logical deduction, the price they charge for the usage of their trademark should be some discount to the increased conversion that can be had if an ad doesn’t have the trademark.

For example, an ad without the trademark has a click-through rate of 2%, but with the trademark it increases to 5%. A life insurance company would line up to pay Oricon money for such a substantial improvement in KPI.

So not only can Oricon raise prices in relation to the effectiveness of their trademark, but they can also almost perfectly price discriminate against companies whose customers have higher LTV (lifetime value). This is similar to how AdSense works on YouTube videos. Channels that make financial videos make way more money per 1000 views than prank videos because insurance/financial companies are willing to pay more to target more affluent viewers. If an individual is looking at video content on TFSA/RRSP/IRA/government tax-advantaged investment accounts, they likely have money to invest.

There could come a time in the distant future when the association can become so strong that the actual credibility of the actual survey might not even matter; there will come a point where slapping an Oricon trademark will lead to increased conversion vs. not having it. Foodies can blindly trust that they will have an excellent dining experience at a Tabelog Gold award-winning restaurant.

Reputation and credibility take a long time to build. Once Oricon becomes highly trusted for its rankings, not only will its trademark encourage consumers to use its product or service, but there will also be no need for another incumbent.

The reputation established through longevity will be Oricon’s competitive moat. No competitor can simply create a customer satisfaction survey with a trademark and attain the results that Oricon has had. Why would customers switch to a ranking list they are unfamiliar with? Why would companies pay to use a trademark from some unestablished company?

My read on the pulse of the situation is that Oricon is still establishing itself as the de facto gold standard in ranking services. For the customer satisfaction survey to perform the way it is currently performing, Oricon must have at least a good reputation in the mind of the consumer, and the trademark has to be working for the trademark contract rates to increase to 39%.

What we hope to happen is for Oricon to generate the same level of credibility it had with music rankings across other service rankings and maybe even expand to product rankings.

They have competition from certain companies, i.e., JD Power (auto, insurance, finance), but Oricon can expand into rankings for all products and services where there is currently no clear winner. i.e., avoid restaurant rankings because Tabelog dominates that ranking list.

Oricon has the potential to become the de facto gold standard for all things rankings, where stamping an Oricon trademark increases the credibility of the firm and hence converts an otherwise suspecting consumer into a customer.

Ranking Lists Business Economics:

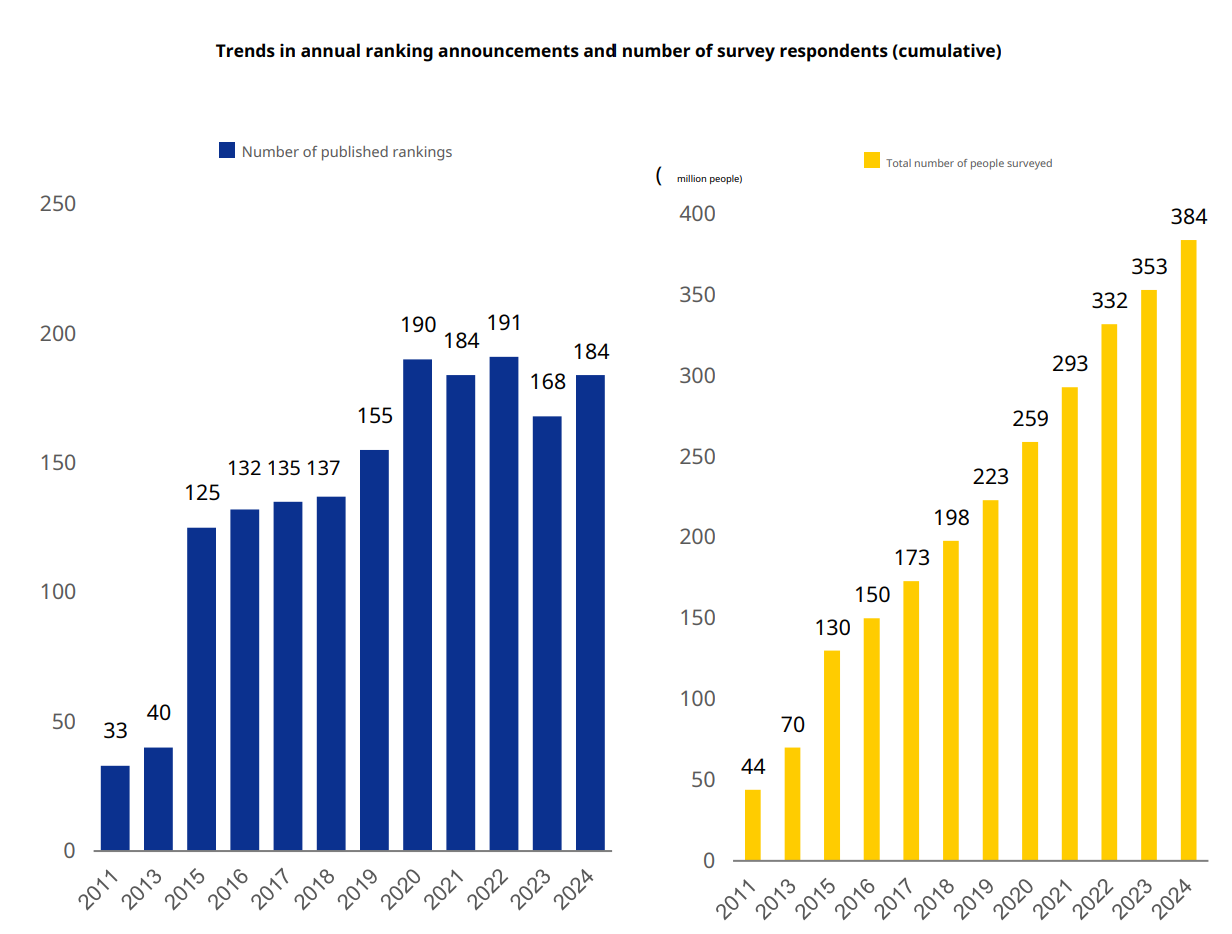

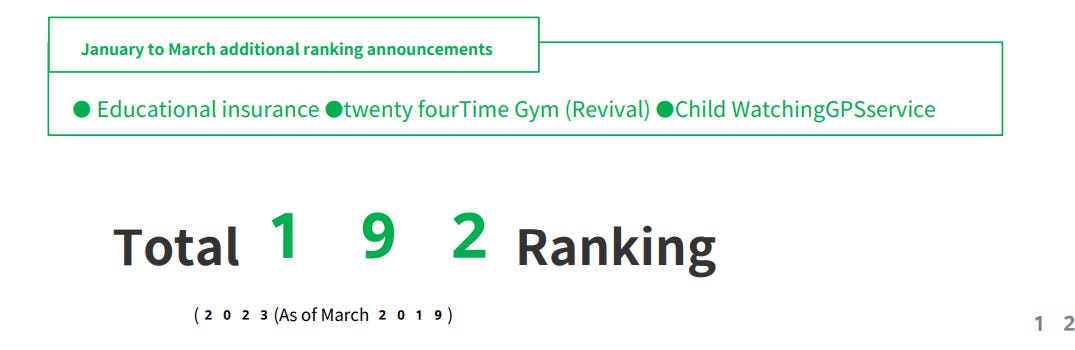

As we can see, there was a decline in ranking lists in 2023. Oricon must spend upfront capital to gather data from survey respondents to conduct these customer satisfaction surveys. Sometimes the data will result in a monetizable ranking list and sometimes not.

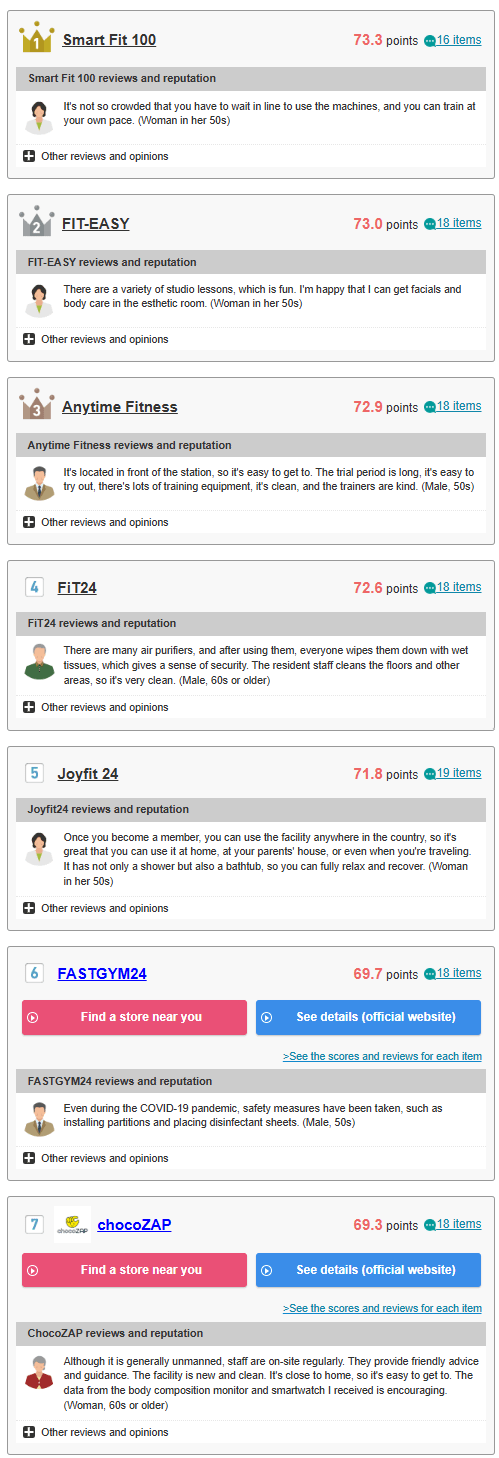

In the following screenshot, it can be seen that Oricon has revived the 24-hour Gym ranking list. Having written a deep dive on Fast Fitness Japan (7092), “Anytime Fitness” was the pioneer of the 24-hour gym chain in Japan; hence, there were very few competitors. After Anytime Fitness proved their business could work, many competitors entered the space, making the competitive landscape more saturated. Given there are more options now, it makes sense for Oricon to revive the 24-hour gym ranking list. Anytime Fitness won in every metric in 2024, but in 2025 AF took 3rd.

Which is to say, even if a ranking list is removed, the work is not completely lost in that it can be revived.

In terms of business economics, the most monetizable ranking lists are where there are high levels of competition, and despite the top 3 being ahead, the underdogs can take market share if the top 3 are not careful. This is where having an Oricon trademark would be very monetizable because the top 3 will want as many advantages in differentiating themselves from their competitors if the service seems similar to the uninformed. i.e., car insurance, real estate brokerage, and cram schools.

What drives each segment are:

Trademark Use KPIs/Op Stats:

# of ranking lists

trademark usage contract rates, %

ARPU—average revenue per contract (user) [not reported, estimated]

Digital Promotion (customer referral rates) KPIs/Op Stats:

Oricon ranking website traffic (not reported, similarweb?)

“Customer referral contract rate” = # of companies signed up for customer referrals/# of companies included in all surveys (not reported)

Click-through rate: When a customer visits a ranking list, how likely are they to click a link? (not reported)

Clicks: Customers pay a variable fee dependent on the number of customers Oricon refers to their companies’ websites. (I am not sure if there is an upfront fee or not.)

Data Distribution KPIs/Op Stats:

# of ranking lists

Note: Newer ranking lists would have less historical data and hence would be potentially less attractive to a buyer, which is to say future sales could improve.

Other (speculated to be consulting) KPIs:

# of clients who are contestants

Driving Trademark Revenue:

*Trademark Revenue = “Avg Implied # of awards that qualify for trademark contracts” x Trademark Usage Contract Rates, % x Avg Revenue Per Contract

**Avg Implied # of awards that qualify for trademark contracts = Avg Ranking Lists x 3 ← 3 being 1st, 2nd, and 3rd place

For the trademark revenue segment, I believe Oricon will continue to increase the number of ranking lists.

But simply increasing rankings lists doesn’t guarantee increased revenues or earnings; what is most important is trademark usage contract rates. 39.1% of winners have contracts. I believe there is still a lot of room to grow here.

The slight dilemma I have here is the No. 1 winner will have the most incentive to sign a contract, but I’m not sure how much incentive 2nd or 3rd place has. Who wants to put on their marketing material that they are 2nd or 3rd? Wouldn’t that advertising simply make a consumer think, I wonder who No. 1 is then?

I guess the wonderful thing about the consumer thinking about who is number 1 from seeing an Oricon trademark logo for 2nd or 3rd is that the consumer will want to visit the Oricon ranking website to satisfy their curiosity.

The counter to the above argument would be in highly saturated services where there is limited availability. If I were looking for a cram school, but the top cram school was fully booked, then I’d look for the 2nd place winner for availability. This could apply to daycares and gyms. Say the No. 1 gym is 15 minutes away and is constantly packed during peak times, but the No. 2 gym is 10 minutes away and not as packed.

I did a thought experiment in my head. I believe the following to be attainable:

95% of 1st place winners sign trademark usage contracts

50% of 2nd place winners sign trademark usage contracts

33% of 3rd place winners sign trademark usage contracts

Blended trademark usage rate = 59.4%

And then, based on price, 1st place winners would pay the most, and 3rd place winners would pay the least. Currently, we have no data on this.

Another element that makes revenue forecasting a little more difficult is the pricing of the trademark. I believe the trademark fee should be different for different industries and services. A 24-hour gym chain with 1000+ locations in Japan would be willing to pay far more for the No. 1 trademark than a hair salon chain with 50 locations in Japan.

The value of the trademark should be tied to the increase in the following metrics:

Click-through rate of an online ad

Increased conversions or organic search from seeing a billboard, marketing material, flyer (harder to gauge)

Can the trademark be the deciding factor that tips the scale in a company’s favour?

What is the value of the product or service being sold?

LTV of the customer

What would be the difference in sales with and without a trademark?

Now that we have established that the trademark fee is dependent on its ability to increase sales performance, then as Oricon’s credibility improves over time, so too will they be able to charge more.

The positive flywheel here is increased credibility, which leads to increased conversions from users of Oricon’s trademark, which leads to Oricon being able to charge more, which leads to more companies signing up for trademark usage contracts.

The current method of driving trademark sales is the best method I can think of given known data.

Hidden Growth Opportunities in Trademark:

Further ranking lists based on age, region, gender

Lower trademark usage pricing for region-specific awards. i.e., if you are No. 1 in the Kanto/Tohoku/Kansai/etc. regions

AI to create customized ranking lists tailored to each user

Create ranking lists for products, in addition to services

Expansion overseas

Adopt business model in overseas markets

Can maybe start off with Japanese offerings that international audiences would value—create a rival to MyAnimeList or MyDramaList, etc.

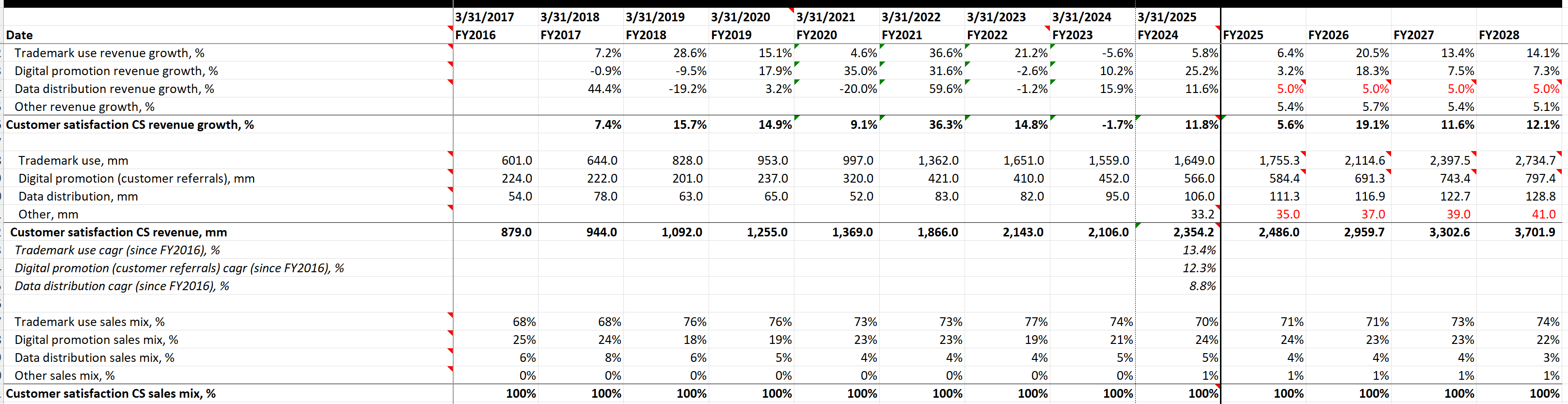

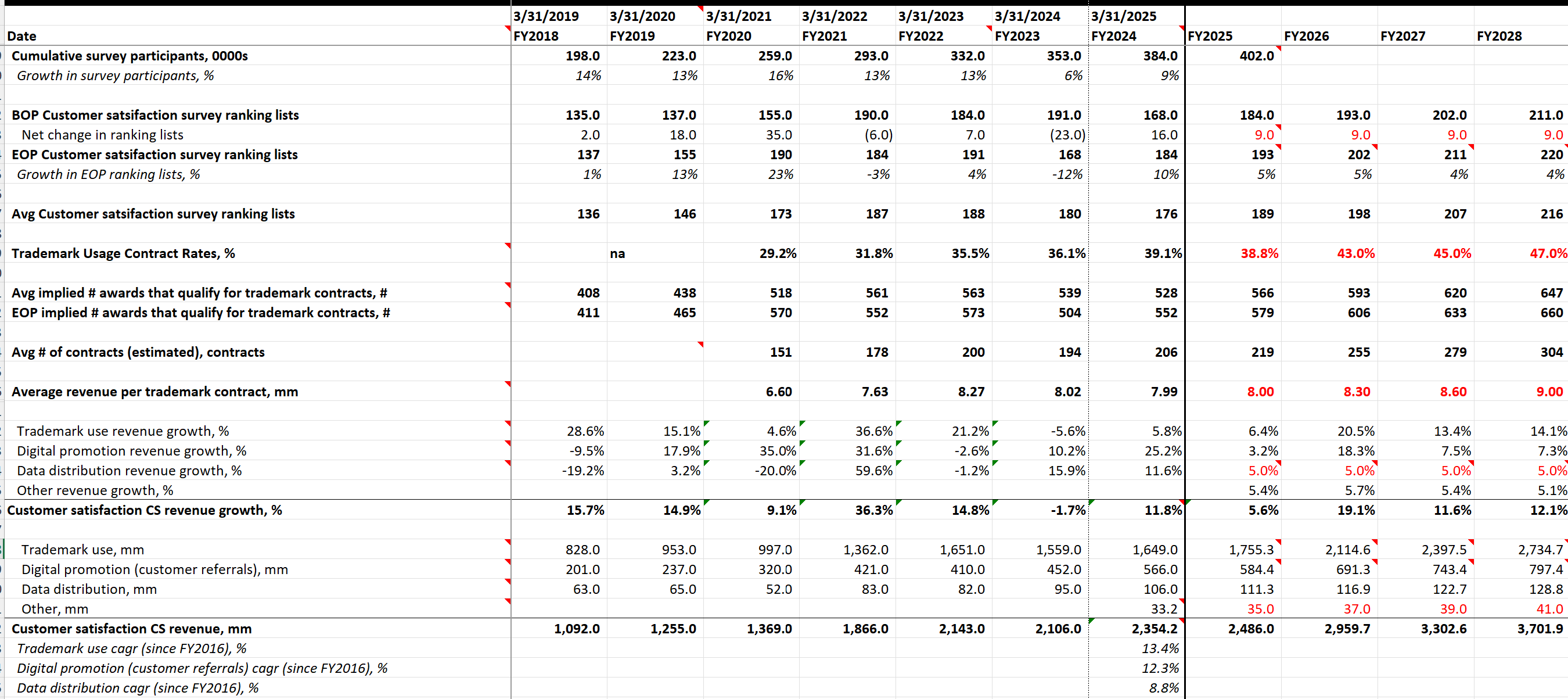

Trademark revenues have CAGRed at 13.4% since FY2016. From all the above growth opportunities, I believe trademark revenues still have a long runway for revenue growth and operating leverage. The current revenue level is due to a shift in ranking lists; once ranking lists resume course, and the positive flywheel compounds over a few more cycles, I believe trademark usage contract rates will increase, and so too will the ARPU.

Limited Time Offer:

Summer Special Promo! 50% Annual Subscription (15 USD/month) → LINK

Summer Special Promo! 30% Monthly Subscription (21 USD/month) → LINK

*Promo ending in 2 weeks.

Digital Promotion (Customer Referral) Segment

Oricon’s rankings are published on its ranking website, where the public can see the companies considered in the survey, the survey questions asked, and the survey results.

In order for a company to directly link their company website to Oricon’s ranking list, they must enter into a customer referral contract, paying Oricon based on the number of customer referrals directed to their company page; hence, the higher the traffic to Oricon’s ranking page, the better.

My interpretation of this is that the companies who sign up are paying a variable fee for this service, so it is different than the trademark segment in that there likely is little to no upfront fee.

The interesting part of this segment is that if there are 10 companies in the survey, linking one’s website is not limited to just the top 3 award winners. All companies can pay to refer customers to their website.

I believe this opens up a large revenue potential for Oricon. Once Oricon rankings become the gold standard for customer satisfaction surveys and organic traffic increases to such a level that it would be suboptimal to not have your link attached to your ranking on the ranking list.

Here is a ranking list where the top 3 winners did not opt for customer referrals, but the two last-place finishers opted in. I have seen other interesting combinations.

Here is the opposite scenario for English schools, where everyone except the 3rd place finisher opted in for customer referrals. By the 3rd place finisher not opting in, they may be losing customers to their other competitors.

If you are a consumer, it’s much easier to click a link than to search in Google for the other companies. There could be a scenario where by not signing up for customer referrals, you are losing customers to the other companies on the list.

I believe customer referral income to be most abundant in ranking lists where companies operate in saturated markets.

Oricon can then bundle trademark usage, customer referrals, data distribution, and consulting in any package to increase ARPU.

Hidden Growth Opportunities:

I believe if Oricon could create tailored ranking lists using AI, then more companies would be incentivized to sign up for customer referrals, because a company on the bottom of the general ranking list might appear on the top of a list for a unique customer.

As we can see from the above, customer referral revenue CAGRed 12.3% since FY2016. Based on all the growth opportunities I listed above, I believe customer referral revenue has not reached its potential.

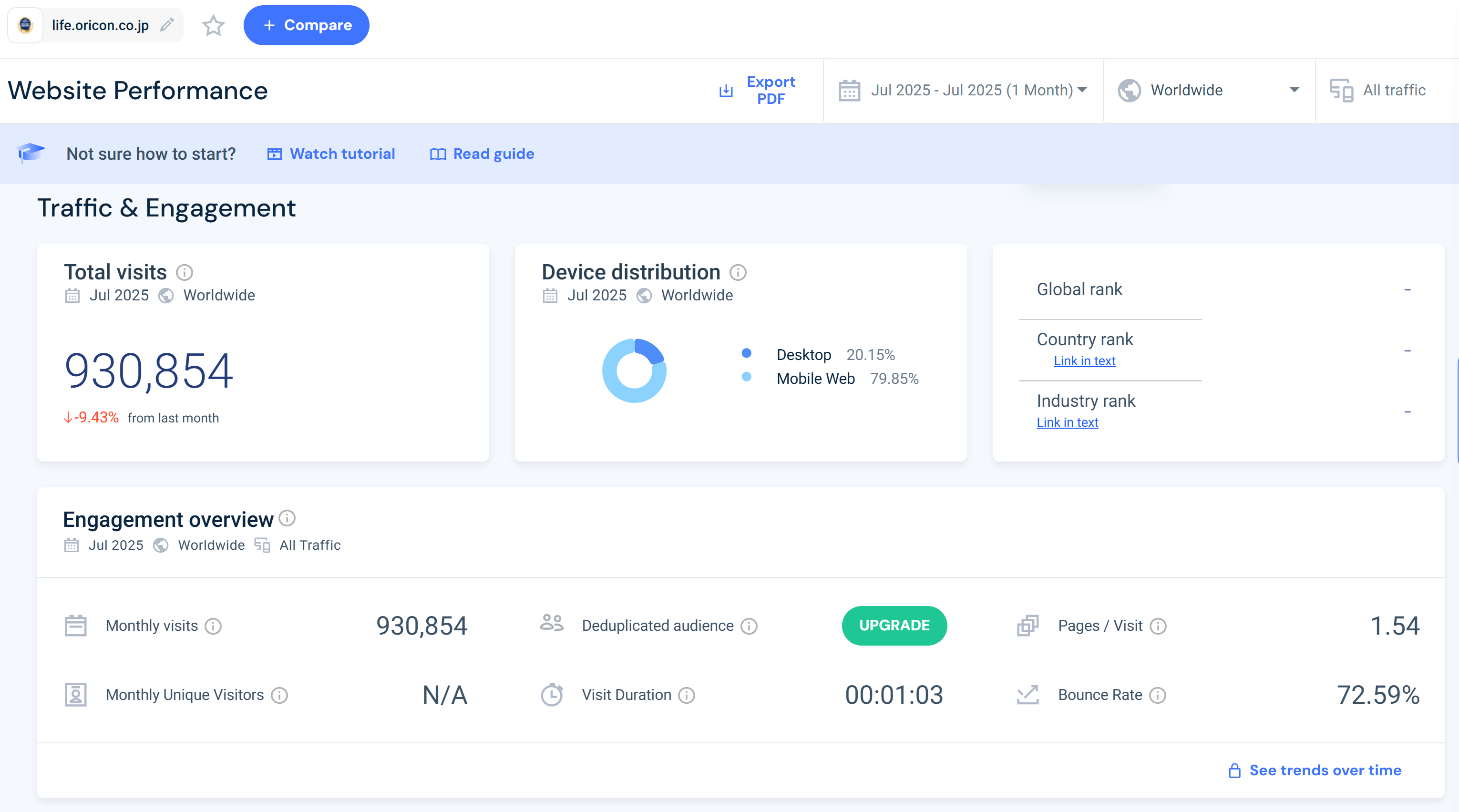

According to Similarweb, Oricon’s ranking website only has 1 mm visitors a month. I believe there is room for visits to substantially increase over time.

Data Distribution:

This segment should increase as ranking lists and companies covered grow. I don’t have high hopes for this segment, but I do believe they will continue to gradually grow.

Other (Consulting):

I am not sure how effective consulting will be as a service, so I’ll reserve comment until more historical figures present themselves.

What’s the upside?

I believe the number 1 case study for Oricon is Kakaku (2371).

Kakaku owns:

Kakaku.com: the No. 1 shopbot website in Japan

Tabelog: the No. 1 restaurant ranking guide/table reservation website in Japan. Replaced Michelin and grew in popularity due to being more representative of what Japanese people think are the best restaurants in Japan, as the ratings are based on real customer reviews.

Job Box: a job search site that has the most job postings (not the No. 1 job search site) in Japan.

other referral services

I believe the Tabelog business to have the highest degree of competitive moat. For most countries, achieving 3 Michelin stars is the highest accolade a restaurant/chef could attain. Michelin was seen as the gold standard for restaurant rankings globally. For Tabelog to dethrone Michelin in Japan is no easy task.

How was this possible? TLDR I could talk multiple paragraphs about this, but essentially Michelin was not accurately reflecting how people in Japan would view a restaurant. Tabelog adjusted their rating system to allow users with more credible eating experiences to sway the ratings. So a person who loves Unagi and has shown on the Tabelog app to have made table reservations at over 50 Unagi restaurants would have way more “influence” on Unagi restaurants than someone who has gone to 2.

Every year Tabelog releases its ranking of Tabelog Gold, Silver, and Bronze winners, which is an accolade similar to Michelin 3-star ratings.

The point I am trying to make is being seen as a “credible” source for referrals, where one’s rankings are seen as accurate and trustworthy, once established, typically results in 1 company, at most 2, dominating public perception.

This can be seen with Oricon music rankings and Billboard fighting for the No. 1/No. 2 spot.

For further discussion on the extrapolations of Kakaku as it relates to Oricon, see the appendix1

Back to valuation, if Oricon becomes the gold standard for rankings beyond where there is overlap, car insurance with J.D. Power, Oricon’s multiple should rerate to something in the vicinity of Kakaku 2371.

Once Oricon reaches Tabelog-level credibility, accuracy, and trust, they can charge more for using its trademark, and margins would further expand. It becomes a license to print money and a tax on any service it covers.

Tabelog is clearly a tax on the restaurant industry in Japan. If you want to offer online table reservations, you go with Tabelog, and you can’t say no to their fees because they control so much of the online traffic for organic restaurant discovery; it would be a suboptimal decision to not be on Tabelog for most restaurants. The only exception is if you are a highly established restaurant that is constantly booked up weeks or months in advance; then Tabelog’s service is not required.

The business economics for utilizing a ranking trademark are phenomenal; the difficulty is in getting there.

It is so easy to miss the mark on exactly what Oricon could be worth in the best-case scenario. It is truly difficult to ascertain, given the upside is so great if exceptional execution and luck are on their side.

Here are some Kakaku valuation metrics over the last 10 years:

LTM EV/EBIT: 11.4x-21.8x

LTM P/E: 20.4x-49.4x

LTM P/B: 7.1x - 16.6x

LTM P/S: 4.9x-10.1x

If we assume the lower end of each of the above metrics:

If we assume no revenue growth or margin expansion from 2026, highly unlikely, here is the return profile:

Sales: 6000

EBIT: 1450

Net Income: 960

BV: 5,657

LTM EV/EBIT: 11.4x *1450 = 16.5 bn yen; add net cash of 3.8 bn; Mcap = 20.3 bn yen

LTM P/E: 20.4x *960 = 19.6 bn yen

LTM P/B: 7.1x*5657 = 40.2 bn yen

LTM P/S: 4.9x*6000= 29.4 bn yen

Based on the company’s current Mcap of 9.9 bn yen, the company could generate a 100-300% return.

Update as of June 2026:

Substack post reviewing their latest earnings

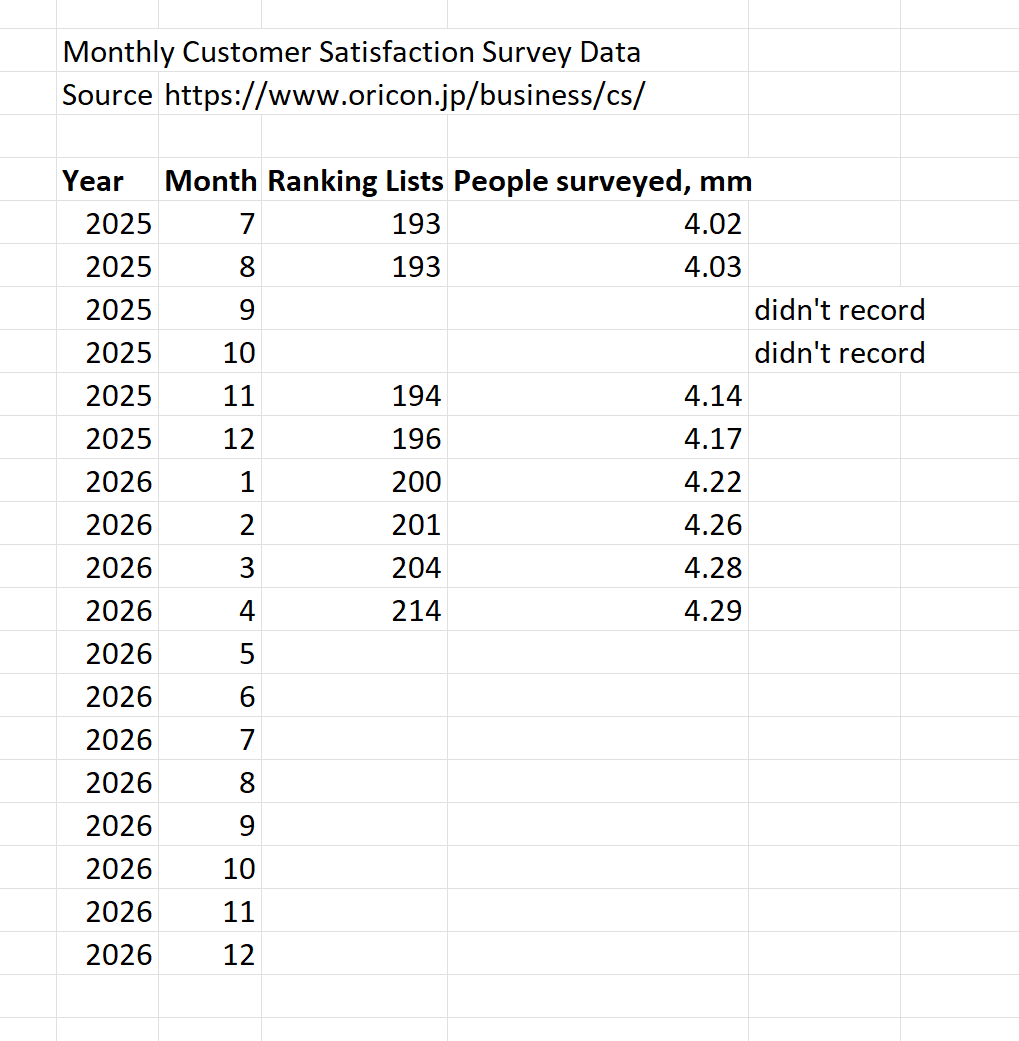

The above is alternative data provided only in the business description section for the customer satisfaction survey business. Every month on the 1st or 2nd, the company will release how many ranking lists and people have been surveyed. If you forget to record it, then it’s gone.

As of May 2026, the company completely stopped reporting both figures. The last update was in April 2026.

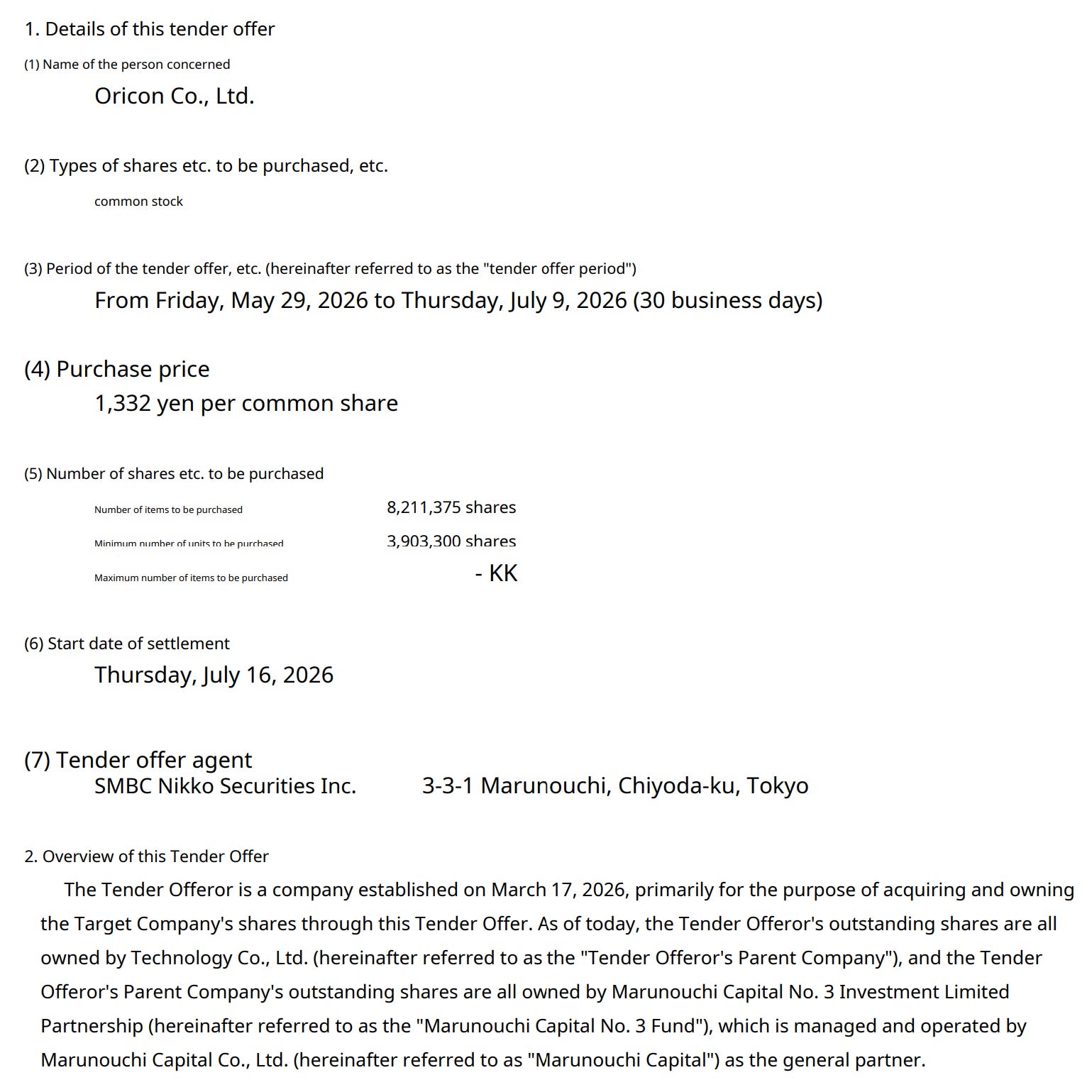

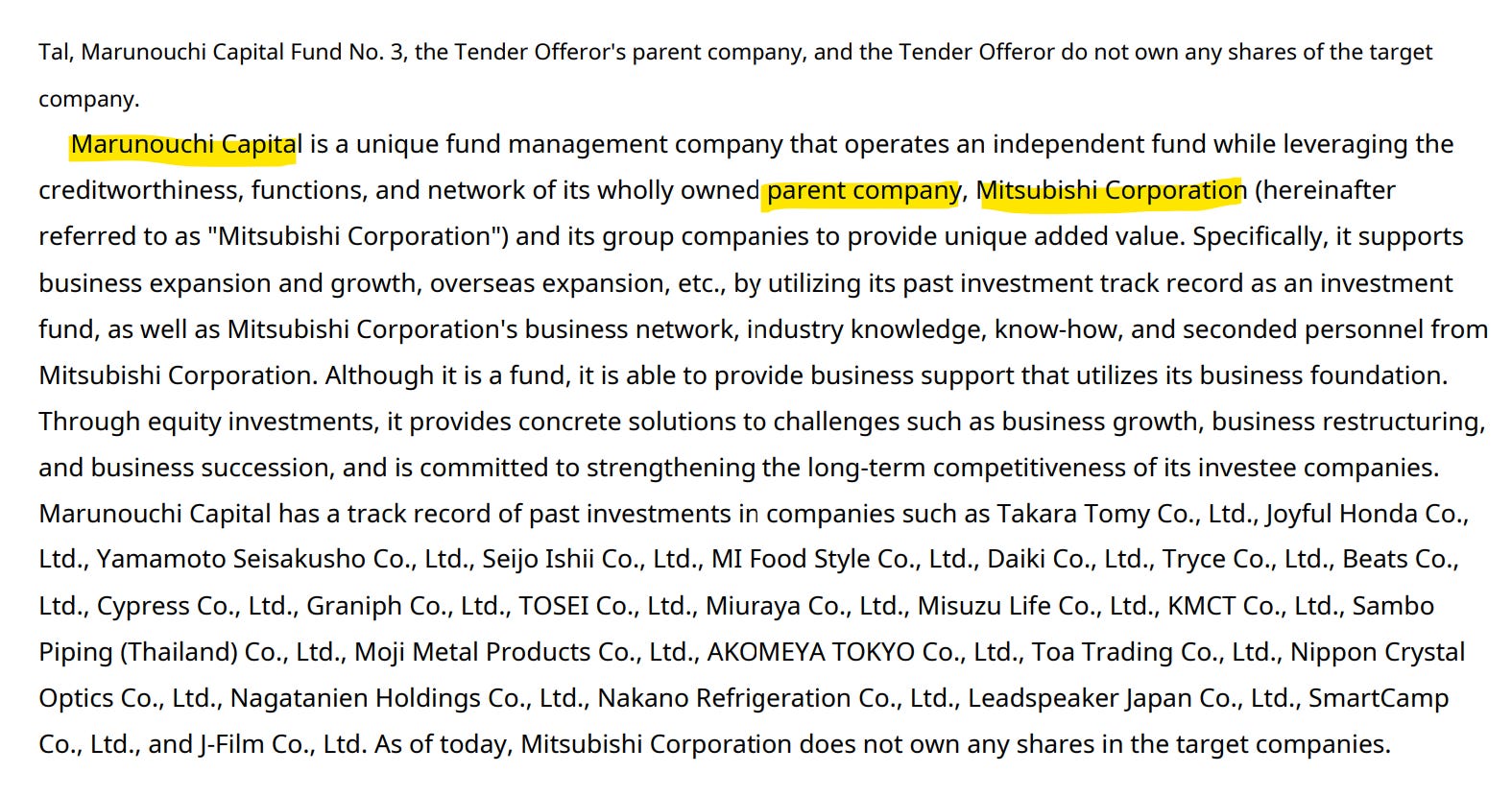

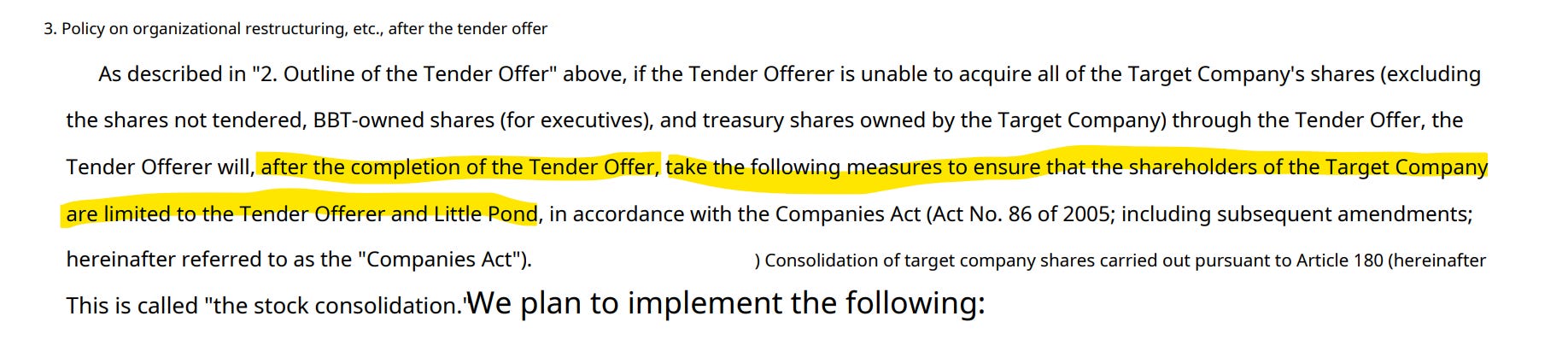

Here are some brief details of the MBO:

I believe the Koike family knows what they are holding onto. I believe the Koike family is carrying forward their economic interest because they know the long-term potential of Oricon. Mgmt’s offer would seem fair to a short-term-oriented investor or an investor that doesn’t understand what they are holding.

At 16x PE, an investor that has an outlook for the company of 1 year would be satisfied with this offer.

But we forget about the 4.4 bn in net cash, including investment securities, on the balance sheet that will certainly be used for debt paydown once the MBO is completed. So the true figure to pay attention to is that Oricon is getting swallowed for 7.7x EV/EBIT.

Although I myself am happy with a 60-70% return in under 1 year, it is bittersweet that it looks like I very much cannot participate in the upside potential of Oricon.

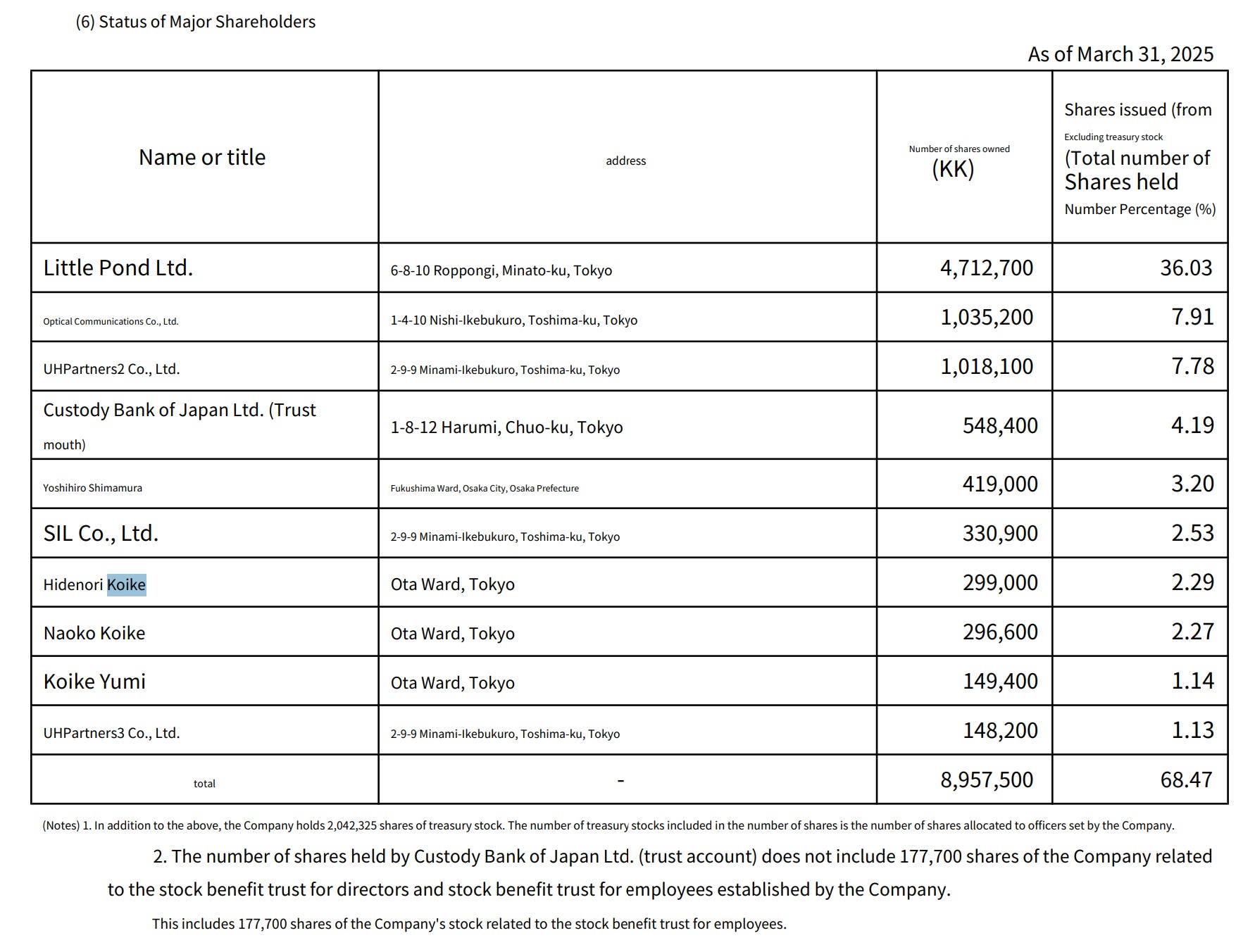

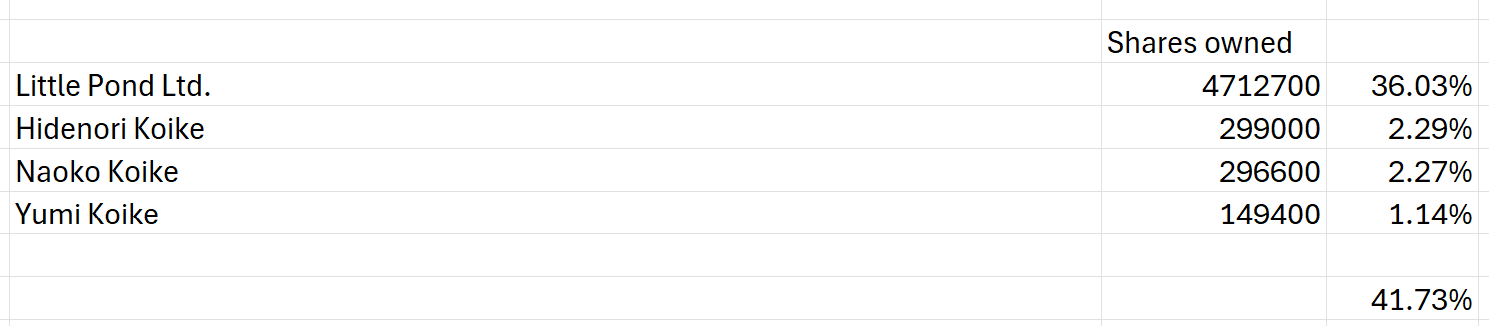

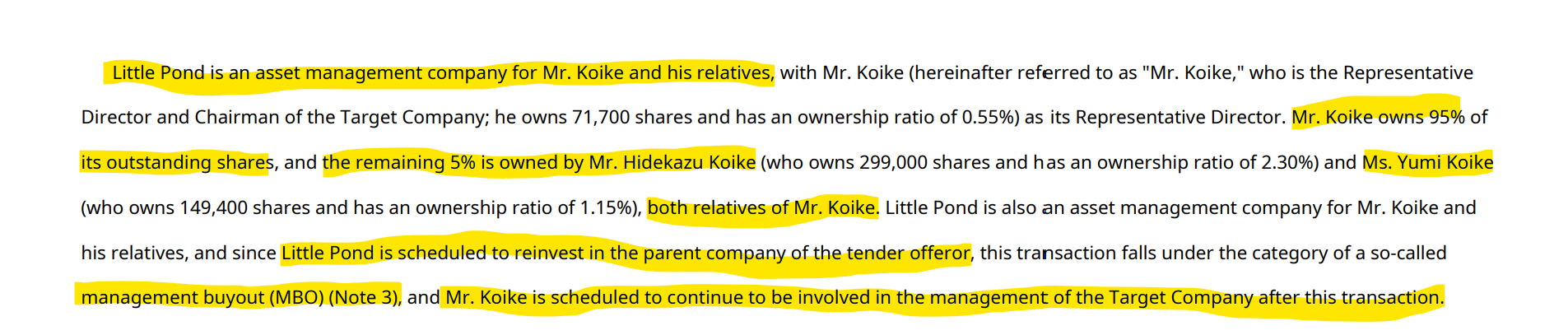

“Little Pond” is (likely a bad translation) a fund made for the benefit of the Koike family. In total, the Koike family owns 41.73% of shares outstanding (net of treasury shares).

Here are additional points from their press release:

So only Little Pond is the surviving shareholder. The shares owned by Hidenori, Naoko, and Yumi are part of the tender.

Given the company plans to acquire up to 8.2 mm shares, the tenderable shares from the Koike family make up 9.1% of target shares or almost 20% of the minimum threshold of shares needed for the MBO to go through.

On the surface, if you didn’t know how to do fundamental analysis or were looking at Oricon for the first time, you would think this is a fair offer. But if we truly factor in the long-term potential Oricon has with its positive flywheel and there being no competitors and the TAM they could service, Oricon is still quite undervalued.

My read on the situation is that they are purposely not releasing May figures because it could potentially indicate that the increase in ranking lists is picking up traction. If the narrative flips to Oricon being a high-growth company, Marunouchi Capital would have to pay more to acquire shares.

This coupled with the conservative FY forecast. I believe given the substantial increase in ranking lists to 214 ranking lists, Oricon should outperform in the next 6-12 months. I think what a buyer would fear is that shareholders start understanding that the narrative has improved and that Oricon will continue to grow ranking lists and achieve a higher contract rate, so they will no longer be able to acquire shares at 1332 yen per share anymore.

What management is doing is acquiring Oricon’s valuation in 1 year and keeping all the upside from 1 year + all to themselves and the private equity fund.

We are likely at the point where the business is about to take off. Surprisingly, mgmt makes up an excuse that they have a lot of capital-intensive investments they want to make, which would work better in a private company structure. I personally don’t buy it.

The company share price, before the stock rallied, was around 800-900 yen per share. I genuinely don’t care if they wanted to be aggressive with capital allocation because I know what Oricon is capable of growing into, which is a Kakaku generalist ranking list company.

How much could their share drop? Oricon is already cheap and has a lot of cash. Mgmt’s justification only applies to short-term holders that care about price volatility but penalizes long-term holders that truly see the value of the company over the next 3 years.

I believe management, by approving this transaction, is not working in the best interest of shareholders but more so for themselves. The fact that they suddenly stopped releasing the May ranking list and survey data indicates that they want to acquire the company before there is factual evidence the company is experiencing its next leg of growth. If the management were not allowed to carry forward their economic interest, I suspect the share price they would negotiate for would be significantly higher.

Given the offer isn’t egregiously bad, it will be hard to fight this in court. I think the only way to remove the MBO is for shareholders who cumulatively own more than 4,308,075 shares to not tender their shares (33.6% of shares outstanding needed to block the deal). I know Hikari Tsushin owns shares (UH Partner 2 & 3, 9% roughly, if my guess is right), so potentially they and other shareholders can join forces.

If anything, even if Oricon gets swallowed, I hope this stock reveal has shown you part of my process and how I read between the lines to find a truly exceptional business.

The next time I reveal that I have a high-conviction stock, make sure to not miss out on potentially truly exceptional gains.

(50% off Annual Subscription ←Click The Link)

This exact thing has happened to me with Shinoken Group, Fast Fitness Japan, and now Oricon. I guess you could say I’m lucky and unlucky at the same time.

I guess a truly S-tier stock is one where you are lucky enough that the stock rallies and somehow doesn’t get acquired…

Thanks for reading! If you’ve enjoyed my research, consider becoming a paid sub!

Continuous Compounding - Alan

Limited Time Offer:

Summer Special Promo! 50% Annual Subscription (15 USD/month) → LINK

Summer Special Promo! 30% Monthly Subscription (21 USD/month) → LINK

*Promo ending in 2 weeks.

Want to read more from Continuous Compounding?

Continuous Compounding Directory/Menu ←click link

Continuous Compounding’s most relevant content all in one place.

Subscribe for free to receive new posts and support my work.

Give Me A Follow On My Other Social Media Accounts:

Twitter ←More active on X than any other platform

YouTube ←SUBSCRIBE! Video Content and Live Streaming. More content to come on this platform.

Instagram ←Not on here much

Reader Exclusive Promo:

Koyfin is my go-to tool for quickly rejecting or diving deeper into potential opportunities. With its intuitive platform, I can:

Instantly access business descriptions.

Analyze valuation multiples and historical profitability.

Review analyst estimates to gauge future prospects.

It’s a huge time-saver for forming a clear, initial opinion on any company. Ready to streamline your research process? Sign up to Koyfin here to save an additional 20% and take your due diligence to the next level!

This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.