Niitaka (TSE-4465): Quick Stock Review

*Legal Disclaimer: This post and all its contents are for informational or educational purposes only. Continuous Compounding assumes no responsibility or liability for any errors, inaccuracies, or omissions in this post, links, attachments, or any actions taken based on its contents. The information sources used are believed to be reliable, but accuracy cannot be guaranteed. Recipients of this research are advised to conduct their own independent analysis and seek professional financial advice before making any investment decisions. The opinions expressed by the publisher in this post are subject to change without notice. From time to time, I may have positions in the securities discussed in this post.

This post and all its contents herein are the exclusive property of Continuous Compounding. This post is intended solely for informational purposes and is not to be distributed, reproduced, or transmitted, in whole or in part, for commercial purposes or sale without prior written consent from Continuous Compounding. Any unauthorized use, dissemination, or sale of this research is strictly prohibited and may be subject to legal action.

Disclaimer: I do not have a position in Niitaka (TSE-4465) at the time of publishing this post.

Niitaka (TSE-4465)

“Quick Stock Review” will be a series of stocks I’ve reviewed in a live stream or done off-stream that could become interesting in the future. This is not a stock pitch, but purely a review of the stock and what opportunities and hurdles the stock has.

Niitaka single stock live stream (recap at 2:10:21):

I figure if a stock has shown up in my stock screen, it may have shown up in yours.

Over time, I’d have such a large archive of quick stock reviews. Most cheap stocks that show up, you can just search my Substack and find a quick summary.

Niitaka specializes in cleaning chemicals catered primarily to restaurants, hotels, food factories, schools, and supermarkets.

The company has recently expanded into the healthcare industry by acquiring a company (Biobank) that sells a lactic acid bacteria-fermented health supplement that aids in digestive health.

Niitaka’s strength is that it is relatively more vertically integrated than its competitors, so it can create custom cleaning solutions for unique use cases for its customers.

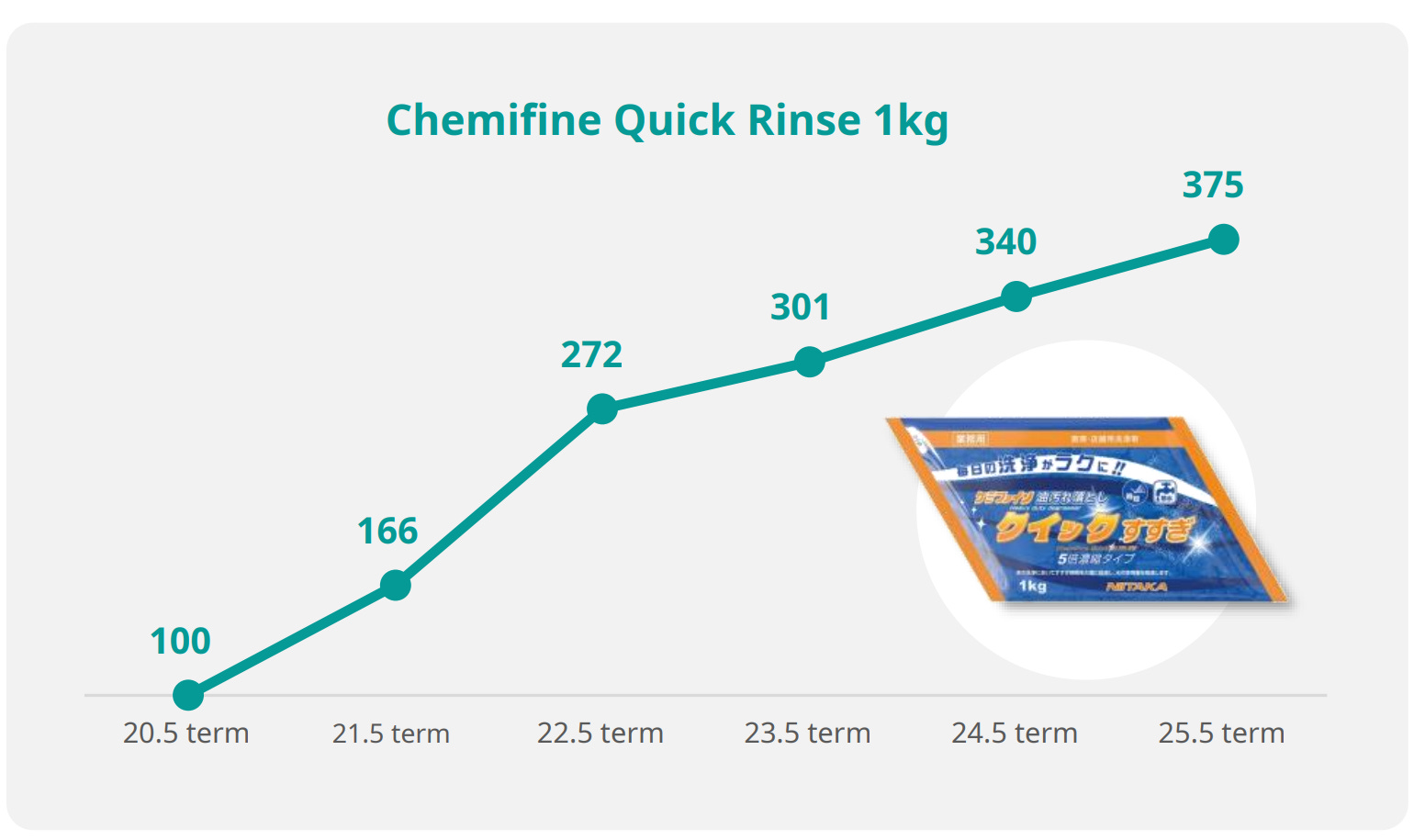

One example is the company’s “Chemifine” quick rinse product. Typically at the end of the workday, restaurants will do a comprehensive clean of all of the kitchen’s surfaces, from the countertops and appliance surfaces to the floor. This is to prevent cross-contamination and ensure floors are safe and not slippery for the next day. Chemifine is a product that doesn’t require scrubbing and doesn’t bubble as much, allowing for faster cleaning times. The primary value prop is that restaurants can save on labour costs with this product due to reduced cleaning times.

Hypothetical example: 6 kitchen staff stay behind to clean the kitchen. With Chemifine you save 10 minutes of cleaning time per person. 60 minutes of labour cost are saved with Chemifine. Would you rather pay a few cents or bucks more for Chemifine or pay more for labour?

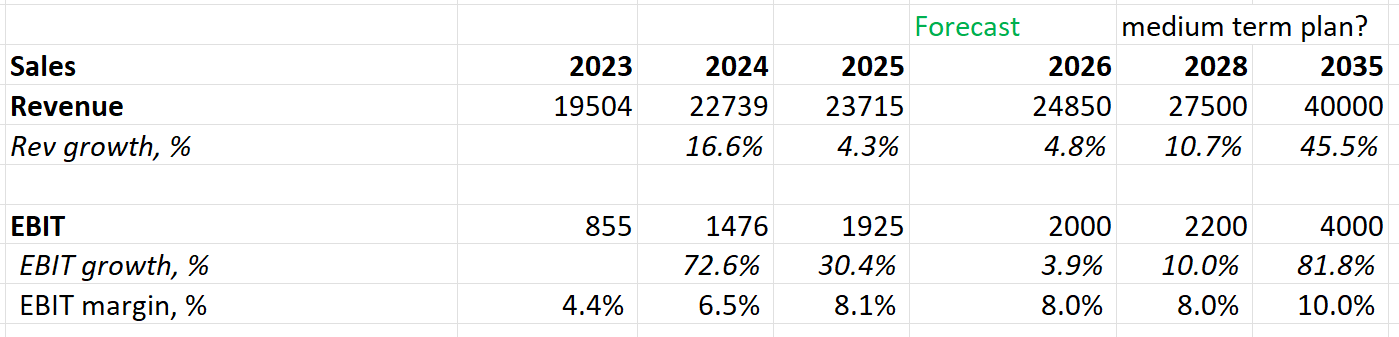

EBIT margins: 5-7%

Revenue growth last 10 years: 65% in total

Valuation:

MCap: 14 bn yen (at 2325 yen per share)

Debt: 1.7 bn yen

Cash: 7.3 bn

Investment securities: 0.5 bn

EV*: 8.2 bn excl. investment securities

EV**: 7.7 bn incl. investment securities

EV*/EBIT: 4.1x

P/B: 0.9x

P/E: 9.2x

Div %: 3.3% (76 yen per share)

Why you would consider investing:

Cheap

Improving margins due to

healthcare products having higher margins than the company’s core business

recent drop in the cost of raw materials

revenue growth as a result of company gaining market share - operating leverage

Gradually capturing more market share in chemical segment

Lots of dry powder to perform more acquisitions in healthcare or related chemical products

Expansion of cleaning solutions for other industries beyond food, i.e., dental clinics.

Food Trends: Trend of eating self-heating hotpot for take-out orders in China - Niitaka sells solid fuels that heat up food over a set period of time while emitting fewer odours.

End customers in restaurant, hotel, and food industries are likely to do well due to tourism boom in Japan

Why you wouldn’t consider investing:

Sensitive to price fluctuations of chemical raw material costs

Cannot completely pass on costs to customers

Circle of competence reasons

No buybacks

CEO owns very little stock, which is interesting

Factor exposure:

Chemical raw material prices: petroleum, natural oils, and fats

Restaurant, hotel, supermarket, and food factory sales

Tourism in Japan

Cleanliness and hygiene standards of restaurants, schools, etc.

COVID would be good for this company given their disinfecting cleaning supplies

Rating: B+/A-

Based on preliminary analysis, Niitaka seems promising. What is most interesting are the levers for growth Niitaka has at its disposal... (content for paid subs)

The following content requires a paid sub, consider supporting my newsletter:

50% off annual paid sub: - link

30% off monthly paid sub: -link

*Offer expires March 22, 2026

**Prices will only go up. This is what my pricing strategy will likely look like, so the earlier you lock in your pricing, the more you save. We are quickly approaching the end of “0-50” pricing. If it overshoots 50 at the end of this promo, I will honour the pricing for those who lock it in.

***There is no guarantee that I will release discounts or what discount rate I choose to use in the future.

The analysis continues below…

Keep reading with a 7-day free trial

Subscribe to Continuous Compounding to keep reading this post and get 7 days of free access to the full post archives.