*Legal disclaimer: The post and all its contents herein are the exclusive property of Continuous Compounding. This post is intended solely for informational purposes and is not to be distributed, reproduced, or transmitted, in whole or in part, for commercial purposes or sale without prior written consent from Continuous Compounding. Any unauthorized use, dissemination, or sale of this research is strictly prohibited and may be subject to legal action. Continuous Compounding assumes no responsibility or liability for any errors, inaccuracies, or omissions in this post or for any actions taken based on its contents. Recipients of this research are advised to conduct their own independent analysis and seek professional financial advice before making any investment decisions.

**Part 1 is more of a pre-acquisition analysis. The main value in Part 1, imo, is the analysis of the new interim CEO’s incentive to sell GAN. Now that we know Sega Sammy is acquiring GAN for $1.97/share, the following is my post-acquisition analysis:

GAN Part 2: Post-Acquisition Offer Analysis

GAN Part 3: SEGA SAMMY PRICE DROP TODAY (Quick Pitch/Update)

GAN Part 4B: Decision Tree Analysis (Factoring Chilean Operation Risk)

*You should read Part 4B before Part 4A. Part 4A was my original decision tree analysis, but I have since factored in Chilean Operation Risk.

GAN Part 4A: Decision Tree Analysis

Literally, my timing couldn’t be better. How could I have timed this so perfectly and imperfectly? I literally wrote this up yesterday. This was going to be my stock pitch for this month…….

If you guys follow me on Twitter, you know I posted about the name 2 days ago.

Then yesterday evening, this happened:

I finished writing the following draft at around 7pm last night, and I went to sleep hoping to edit the rough draft this morning. I woke up seeing my position go up 90%+.

Yesterday’s draft:

$GAN is trading at $0.89 per share.

Mkt Cap=42MM (@ $0.93/share)

Cash: 43mm

Debt: 42mm (incl. operating lease liab.)

EV:40mm

Brief Overview:

GAN is an iGaming and sports betting platform provider. During the iGaming and sports betting boom, GAN gained traction as an iGaming (internet gambling) B2B business. GAN allowed US casino operators to quickly capture iGaming market share following the legalization of iGaming on a state-by-state basis in the US. Soon after their IPO in 2020, GAN acquired Coolbet which expanded their platform offering to iGaming and sports betting. Furthermore, GAN provides a one-stop shop for signing up new users, linking existing casino members to their platform, payment processing, linking rewards/loyalty points already existent at the physical casinos to be used online, data analytics, and many more supplementary services. GAN could also custom-design content/games/UX design and make the platform unique to your casino brand.

Value Proposition:

Imagine you are a 60+ year old casino owner. The states in which your casino operates have legalized iGaming and online sports betting. You have established a loyalty program at your physical casinos. You want to establish an omnichannel presence. You are too old to learn new tricks and don’t really have the expertise to build out an online gaming platform on your own. You hear about GAN and realize that while competitor casinos are attempting to build a platform from scratch, you can have a first-mover advantage by simply working with GAN. GAN’s platform is approved and meets local regulatory requirements, while your competitors still need to be approved.

This value proposition, coupled with the meteoric valuations of any company that had iGaming and sports betting, resulted in GAN trading at $30/share at its highs.

GAN Today:

Now fast-forward to the present year; the hype has died down, and the rapid growth shareholders expected is not present. Revenue growth is not what is expected.

The company now trades at 1/30 of its all-time high.

The current valuation of roughly $40mm EV has me puzzled.

Despite burning cash, can you really create a ready-to-go one-stop shop iGaming and Sportsbook B2B business for $40mm? (not even looking into the B2C portion, they can stop operations, sell it, whatever)

If I'm a medium-cap casino operator with no current buildout, this seems like an easy acquisition to expand my omnichannel reach. This is simply taking the company to use for myself. If I want to further juice it, I can start offering the tech to other operators in regions where I don't operate to avoid any conflict of interest. A deleveraged CNTY could be a buyer, for example.

Furthermore, if I am a current client of GAN, instead of paying GAN revenue/profit share, why don’t I just buy them out?

If I’m a casino operator, I don’t intend to start an iGaming and sports betting omnichannel offering and suddenly decide to stop completely. So I can either continue with GAN or create my own offering later down the road. GAN signs 3-5 year contracts with clients. Wynn signed a 10 year contract in 2020 so they will receive revenue from Wynn until roughly 2030.

So let’s say I’m a client and I pay GAN $5mm a year. I asked a software engineer friend of mine that it would take $20mm to make the iGaming and Sports betting segment. This is very surprising to me. I didn’t think it would be this cheap.

Prior to their acquisition of Coolbet, the company had capitalized 26.5mm in software development costs, with 2.6mm in progress, so this was around the ballpark. Thus the iGaming platform was built for around $29mm.

So why do we use GAN and not build?

Speed. First mover advantage

Less of a headache

Why do we leave GAN and create our own?

Potentially higher level of customization

Get to oversee all aspects of the gaming experience (UX) and product offering

Cheaper in the long run

Higher levels of privacy. Performance figures and data analytics are kept exclusive to one’s own company. Whereas you share your performance with GAN.

Here is a historical record of capital raised:

“On May 7, 2020, GAN Limited completed its U.S. IPO under which it sold an aggregate of 7,337,000 ordinary shares at a price per share to the public of $8.50 and raised gross proceeds of $62.4 million (net proceeds of $55.3 million).” (424B4 5/5/2020) There were roughly 29mm shares outstanding after the IPO. Providing the company with a market cap of roughly 250mm.

A couple months later:

“On November 15, 2020, we entered into a Share Exchange Agreement with Vincent Group p.l.c., a Malta public limited company doing business as “Coolbet.” Under the terms of the Share Exchange Agreement we will offer to acquire all of the outstanding equity in Coolbet in exchange for an aggregate of €149.1 million (approximately $175.9 million), on a cash-free, debt-free basis, which is expected to be paid in a combination of €80 million (approximately $94.4 million) in cash and €69.1 million (approximately $81.5 million) in GAN Limited ordinary shares, subject to adjustment as provided in the Share Exchange Agreement.”

The acquisition of Coolbet would allow GAN to add a sports betting engine to its B2B platform product and service offering. On paper, this sounded spectacular and synergistic. In addition, they could now have B2C operations in Europe and Latin America. R&D for your B2C operations and apply the same tech to B2B; and vice versa. Cost synergies on paper.

To raise cash for the cash portion of the transaction, they performed an offering at $15.50 per share. The pro-forma shares outstanding post-this transaction were 37mm. The market responded by seeing this acquisition as hugely synergistic, as the market price per share never dropped below $15.50. By Feb 2021, the shares had reached $30+/share. The market cap at that time would be approx. $1.1 billion.

We can now acquire GAN, formerly IPOed in the US at a market cap of $250mm, and Coolbet valued formerly at $176mm, for $40mm…..

For the next 1-2 weeks, I hope to answer the following questions:

What is the replacement cost of GAN’s B2B business?

What is the replacement cost of GAN’s B2C business?

What is the sum of parts valuation of GAN?

If I figure out that the sum of parts exceeds the current enterprise value of 40mm, then I am investing in GAN so that they can be sold in the near term. Does this near-term catalyst exist? We’d be sitting ducks if management didn’t want to sell and drive the business into the ground.

From studying the most recent 8Ks, the compensation package offered to the new interim CEO Mr. McGill demonstrates the company has every intention to sell and the CEO is incentivized to sell GAN asap.

Analysis of Interim CEO’s compensation package:

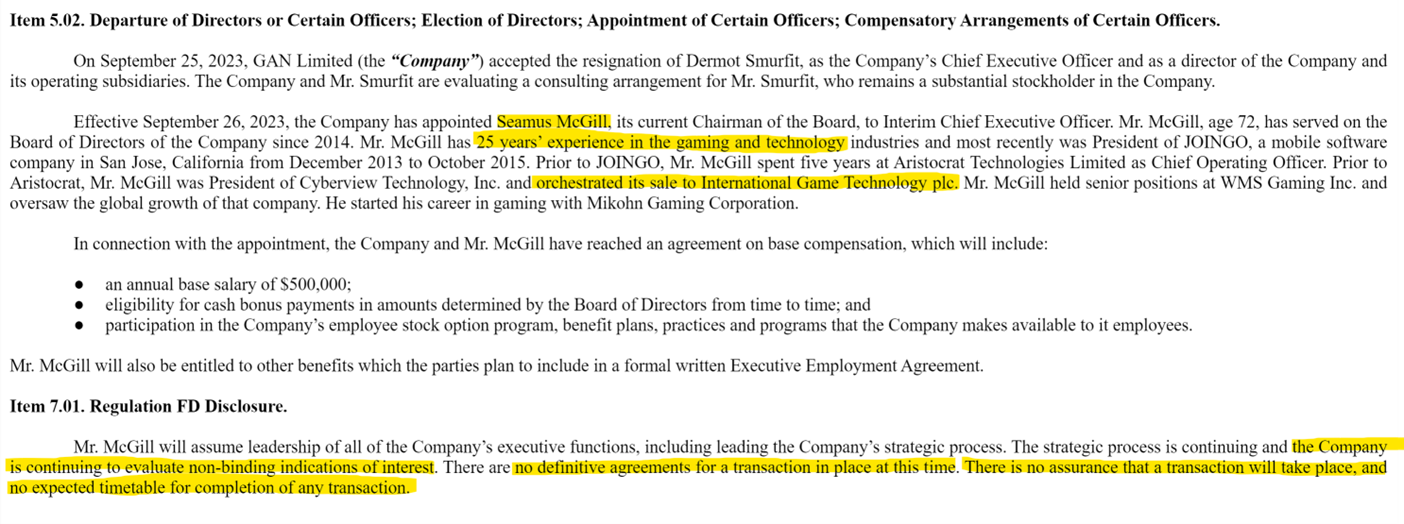

9/26/2023 8-K:

The newly appointed interim CEO is Seamus McGill. He has experience in the space and what stood out to me was that they highlighted that he orchestrated the sale of Cyberview Technology, Inc. to IGT. Also, the company will be evaluating non-binding indications of interest, which means they are looking for a buyer.

10/10/2023 8-K

In October, Mr. McGIll’s compensation incentivizes him to sell the company. The sooner, the better. Here is McGill’s compensation under the following scenarios:

Sold @ 1 year, and terminated without cause:

Employment income:

1. Base salary of $500k

2. Bonus of up to 100% of base salary, +$500k potentially (cash or stock) (min:$0, max: $500K)

3. Since @ 1 year, 25% of 275,000 shares have vested, hence 68,750 shares vest

Severance package:

1. Severance equal to 12 months of base salary: $500k

2. All of Mr. McGill’s remainder equity awards shall accelerate and become fully vested, non-forfeitable, and exercisable: 206,250 * $/share.

3. Transaction bonus: $500k

Total comp min: 500 + 0(no bonus) + (68.75k shares* $/share) + 500 + (206.25k shares* $/share) + 500=1.5mm + (275k shares* $/share)

Total comp max: 500 + 500(max bonus) + (68.75k shares* $/share) + 500 + (206.25k shares* $/share) + 500= 2.0mm + (275k shares* $/share)

Sold @ 1 year mark, and not terminated:

Employment income:

1. Base salary of $500k

2. Bonus of up to 100% of base salary, +$500k potentially (cash or stock)

3. Since within 1 year, no equity awards have vested yet or 25% if exactly 1 year mark

Additional terms:

1. No severance

2. Since Mr. McGill didn’t get terminated, his initial equity award vests following a normal vesting schedule

3. Transaction bonus: $500k

Total comp min: 500+0+(68,750 shares* $/share)+0+0+500= 1.0mm + (68,750 shares* $/share)

Total comp max: 500+500+(68,750 shares* $/share)+0+0+500 = 1.5 mm + (68,750 shares* $/share)

Total comp min: 500 + 0(no bonus) + (68.75k shares* $/share) + 0 + (0k shares* $/share) + 500= 1.0mm + (68.75k shares* $/share)

Total comp max: 500 + 500(max bonus) + (68.75k shares* $/share) + 0 + (0k shares* $/share) + 500= 1.5mm + (68.75k shares* $/share)

Sold in 3 months, and terminated without cause:

Employment income:

4. Base salary of $500k= $500k*(3/12 months)=$125K

5. Bonus of up to 100% of base salary, +$500k potentially (cash or stock) (min:$0, max: $500K)

6. Since less than 1 year, 0% of 275,000 shares have vested

Severance package:

4. Severance equal to 12 months of base salary: $500k

5. All of Mr. McGill’s remainder equity awards shall accelerate and become fully vested, non-forfeitable, and exercisable: 275k shares * $/share.

6. Transaction bonus: $500k

Total comp min: 125 + 0(no bonus) + (0k shares* $/share) + 500 + (275k shares* $/share) + 500=1.125mm + (275k shares* $/share)

Total comp max: 125 + 500(max bonus) + (0k shares* $/share) + 500 + (275k shares* $/share) + 500= 1.625mm + (275k shares* $/share)

From the above analysis of the different scenarios, it should be concluded that Mr. McGill is incentivized to sell the business as soon as possible. Typically, when there is a change of control, the CEO gets replaced, hence a “termination without cause.” The compensation structure is structured in a way that shows the intentions of McGill and the board of directors to simply have McGill come in to assist with the sale of the business.

Furthermore, the compensation structure doesn’t penalize McGill for attempting to sell the business and failing, as his initial equity award fully vests under any termination without cause. So if the board wants to hire someone else to sell the business, McGill gets a $500k severance and 275k shares to ride the upside of a new CEO being better than him at selling the business. This incentivizes McGill to not stay longer than he needs to, and the business can be sold in a timely manner.

No sale in 3 months, and terminated without cause as the board wants to try a different CEO:

Employment income:

7. Base salary of $500k= $500k*(3/12 months)=$125K

8. Bonus of up to 100% of base salary, +$500k potentially (cash or stock) (min:$0, max: $500K)

9. Since less than 1 year, 0% of 275,000 shares have vested

Severance package:

7. Severance equal to 12 months of base salary: $500k

8. All of Mr. McGill’s remainder equity awards shall accelerate and become fully vested, non-forfeitable, and exercisable: 275k shares * $/share.

9. Transaction bonus: $0k

Total comp: 125 + 0(no bonus) + (0k shares* $/share) + 500 + (275k shares* $/share) + 0= 625k + (275k shares* $/share)

*Let’s assume if he doesn’t find a buyer, the board won’t be happy with his performance, hence swapping him out for someone else and there being no bonus.

CEO compensation and what I want as a shareholder are aligned. I have yet to determine if the business is worth operating as a going concern.

Disclosure: I currently hold no position in GAN, Gan Ltd.

GAN Part 3: SEGA SAMMY PRICE DROP TODAY (Quick Pitch/Update)

GAN Part 4B: Decision Tree Analysis (Factoring Chilean Operation Risk)

*You should read Part 4B before Part 4A. Part 4A was my original decision tree analysis, but I have since factored in Chilean Operation Risk.

GAN Part 4A: Decision Tree Analysis

Thanks for your support!

To stay up-to-date or receive notification of when I release my latest stock pitch, please follow:

Twitter: https://twitter.com/compoundersEX

Instagram: https://www.instagram.com/compounders.ex/

YouTube: https://www.youtube.com/@continuouscompounding

Want to enjoy paid memberships for free? Help me grow by referring a friend!

1. Share Alan’s Substack: Continuous Compounding.

When you use the referral link below or the “Share” button on any post, you'll get credit for any new subscribers. Simply send the link in a text, email, or share it on social media with friends.

2. Earn benefits. When more friends use your referral link to subscribe (free or paid), you’ll receive special benefits.

Get a 1 month comp for 1 referrals

Get a 3 month comp for 5 referrals

Get a 6 month comp for 10 referrals