GAN Part 4A: Decision Tree Analysis

GAN Part 4A: Decision Tree Analysis

Making sense of the recent decline in price

*Legal disclaimer: The post and all its contents herein are the exclusive property of Continuous Compounding. This post is intended solely for informational purposes and is not to be distributed, reproduced, or transmitted, in whole or in part, for commercial purposes or sale without prior written consent from Continuous Compounding. Any unauthorized use, dissemination, or sale of this research is strictly prohibited and may be subject to legal action. Continuous Compounding assumes no responsibility or liability for any errors, inaccuracies, or omissions in this post or for any actions taken based on its contents. Recipients of this research are advised to conduct their own independent analysis and seek professional financial advice before making any investment decisions.

***This is the old Part 4: Decision Tree Analysis post. I have revised my decision tree model by factoring in risk in GAN’s operations in Chile. Read this new post instead:

GAN Part 4B: Factoring Chilean Operation Risk

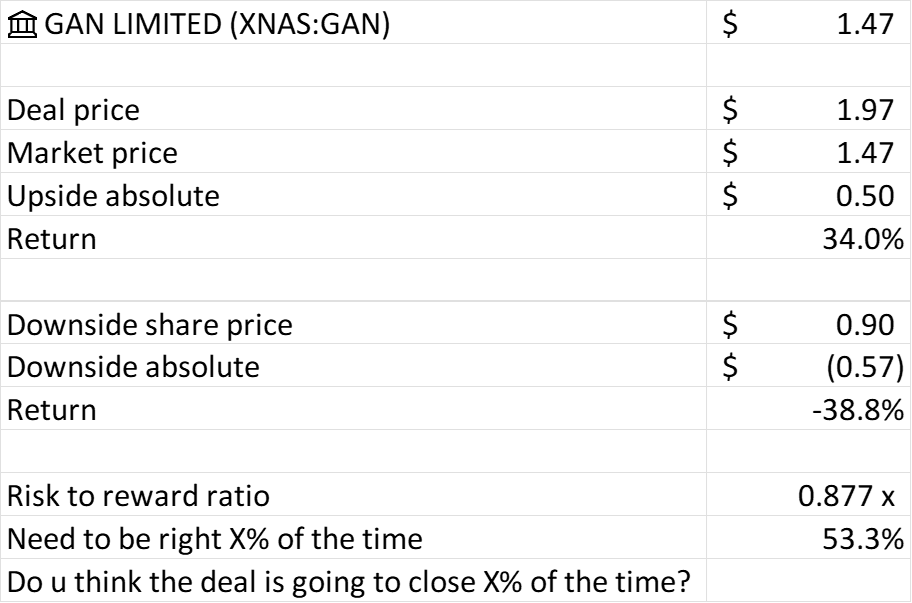

At yesterday’s close (Nov 15th), GAN traded at $1.47 per share. This offers a roughly 34% annual return if shareholders approve of the deal and regulatory approval is attained by Q4 2024.

Based on a $0.90 per share downside price, we only need to be right 53% of the time for this bet to break even.

This is a very simple analysis, so I opted to perform a decision tree analysis and calculate the expected value based on what I believe are the potential possibilities of each branch of the decision tree.

Decision Tree Analysis:

*The Excel model is available to paid subscribers and will be sent via a different post that only paid subs have access to.

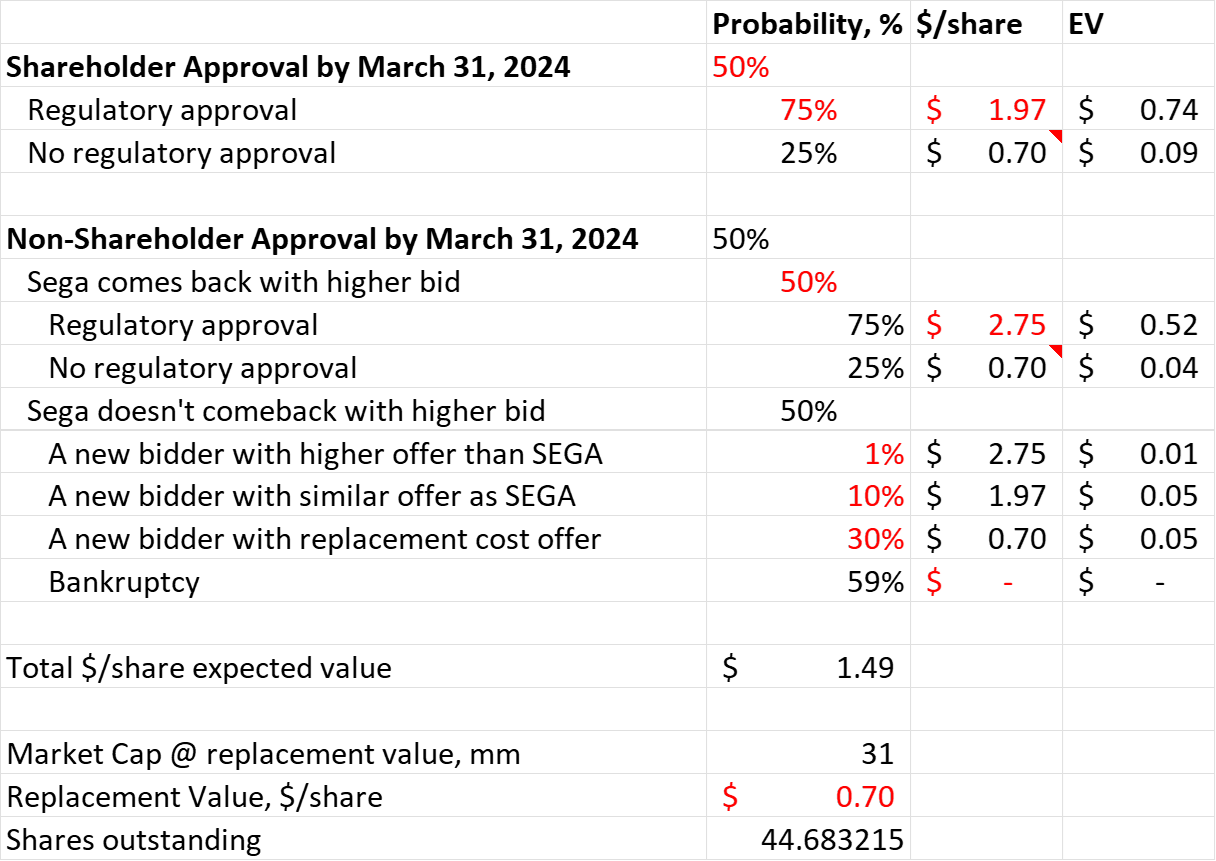

Let me explain what you see in the above table:

Shareholder approval by March 31st, 2024:

There is an assumed 50% chance of shareholder approval by March 31st, 2024

Following approval, there will be a 75% chance SEGA’s takeover of GAN is approved

If not approved, shares drop to replacement value, and the company is acquired at that price.

Non-shareholder approval by March 31st, 2024:

There is a 50% chance of non-shareholder approval by March 31st, 2024

Given non-shareholder approval, it is assumed that, with a 50% probability, Sega will come back with a higher offer price.

Again, probability of regulatory approval is assumed to be the same in the shareholder approval and non-approval scenarios.

I believe if Sega were to raise their offer, they could raise it to $2.50–$3.00. There is nothing academically rigorous about this estimate. The logical step-up from 90mm EV is to $110-130mm EV or $2.50 - $3.00/share range.

If SEGA walks away, then:

There is a 1% chance there is a higher offer

10% chance of a similar offer

30% chance of a replacement cost offer at $0.70

59% chance of going bankrupt.

*Replacement cost of $0.70/share or EV of 30mm

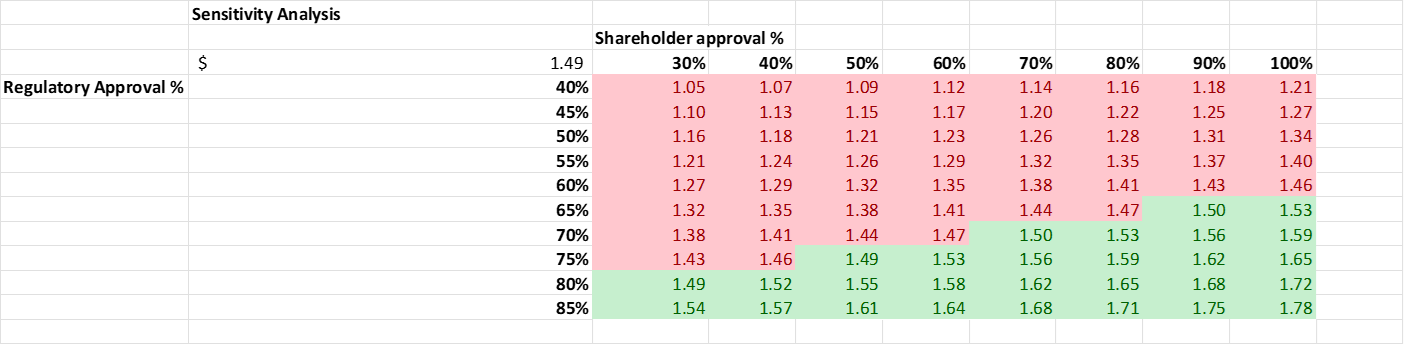

Sensitivity Analysis:

Here is a sensitivity analysis of changes in “Shareholder Approval Rate %” and “Regulatory Approval Rate %”

Let’s see what set of assumptions allows us to arrive at the $1.47 price at the Nov. 15th close price.

Based on the above sensitivity analysis, we arrive at $1.46 roughly if shareholder approval drops to 40% in March 2024, while keeping regulatory approval at 75%

If shareholder approval increases to 60% in March 2024, but regulatory approval drops 70%, then we arrive at $1.47 as well.

If shareholder approval increases to 80% in March 2024, but regulatory approval drops 65%, then we arrive at $1.47 as well.

What I believe reality could look like:

*I do not have a law degree. I don’t have a wealth of knowledge looking at regulatory approval rates. Please do your own due diligence before investing.

One article that I recently read that was very interesting was “The Antitrust Inflection” written by Yet Another Value Blog

In the above article, Andrew Walker emphasizes the success of merger arbitrage in recent cases like ATVI and HZNP, where regulatory challenges presented an opportunity for significant returns. The author suggests that the market has been pricing such cases at roughly 50/50 odds, while they believe a more in-depth analysis would reveal better chances of success. The key argument revolves around a perceived change in the regulatory landscape. The author contends that the government is now more willing to pursue marginal antitrust cases, leading to a shift in market dynamics.

What Andrew wrote is happening to GAN, where the market is pricing the odds of the deal going through at close to 50%.

Regulatory Approval Analysis:

In Part 3 of my GAN analysis, I broke down the variables that would be accessed to determine if SEGA would be given regulatory approval. In summary, here are my thoughts:

Antitrust and Competition Laws:

Analysis:

GAN is losing money. Not that competitive to begin with. SEGA is taking a risk by trying to revive GAN; there is no indication that a monopoly will be formed if SEGA acquires GAN, nor is SEGA’s acquisition of GAN anti-competitive.

SEGA entry into the market could inspire other companies with an IP portfolio to enter the iGaming market. This would increase the content quality as a whole to consumers and consumers would benefit from being entertained with better games

National Security Concerns:

Analysis:

Nothing GAN does is a national security threat. You can maybe argue about user data. Relations with the US and Japan aren’t bad. If this were a Chinese company, then I’d agree; this would be risky.

Market Share and Dominance:

Analysis

SEGA is completely new to the iGaming world, so they have 0% US iGaming market share. GAN is a small fry in the iGaming market. Market share doesn’t increase if an acquisition is approved. They just have a better ability to gain market share when combined.

I do not believe they will dominate the market. SEGA needs to still figure out how to blend its IP portfolio into iGaming games. This has not been figured out yet.

Consumer Impact:

Analysis:

As I mentioned earlier, quality and consumer choice improve as SEGA has the capacity to provide higher-quality iGaming content with better game design and nostalgic characters

I don’t see any negative consumer impact.

Financial Stability and Viability:

Analysis:

If GAN is left on its own, it will be financially unstable. SEGA has lots of cash and more cash than debt. They are investing 100 billion yen in the next 3 years. GAN will be very financially stable with SEGA’s support.

Compliance with Gaming Regulations:

Analysis:

GAN is already in compliance with gaming regulations in each state it operates in. Post-acquisition surviving company/subsidiary will retain the name GAN.

Data Protection and Privacy:

Analysis:

GAN and Sega, as separate entities, to the best of my knowledge, have not had security breaches and have years of experience securing and protecting customer data.

Employee Welfare and Labor Laws:

Analysis:

Given that SEGA has teams across the US, Europe, and Asia, I suspect part of GAN’s workforce will be terminated, including the CEO.

In summary, based on the above, I believe it is more likely that the acquisition of GAN by SEGA will be approved by regulatory authorities. I believe conservatively that the approval rate is likely 85% and realistically 90%+.

At 50% shareholder approval and 85–90% regulatory approval, we arrive at $1.61 to $1.67 per share.

What is the Shareholder Approval %?

This is hard to determine unless we did an online poll with GAN shareholders, but I don’t have enough influence or followers to determine this.

Now here is my beef with assuming shareholders don’t approve of the shareholder bid. Most of the downside scenarios are averted if shareholders simply approve of the $1.97 offer price.

So if you are a shareholder and you fear the potential of shareholders not approving and there being no new bidders leading to bankruptcy or low-ball bidders leading to prices dropping to replacement value, then simply take the deal.

So in essence, those who believe in the most pessimistic case will sell their shares to those who believe in the optimistic case to avoid capital loss or vote for the deal to be approved. Those who believe in the optimistic case will vote for approval. So as shares change hands from non-believers to believers, the odds in favor of the deal being approved increase.

There are a lot of shoulda, coulda, wouldas. People can be emotional and irrational. What happens if a majority of shareholders want more money? For those who believe $1.97 is too low and want to disapprove in hopes of SEGA coming back with a higher offer, that would be a high-risk, high-reward strategy.

This strategy makes sense for long-term bag holders who have large losses. If you are experiencing -70%+ losses (picked an arbitrary number), then you might not care if the stock goes to 0, you just want to gamble the remainder shares you do have. From that perspective, then there have to be quite a few bag holders for them to make a majority.

I am not sure what the right shareholder approval probability rate is, but I believe the mix of shareholders who want to approve and those who don’t want to approve will change leading up to the final decision. If any of my readers have a large following, maybe ask your followers what decision they would vote for.

Summary:

Hence, one should purchase shares of GAN at $1.47 primarily if:

One believes regulatory approval will be higher than 75%

If the probability of shareholder approval is greater than 50%

If you believe Sega will come back with a higher bid that is equal to or greater than $2.75 per share

In the unfortunate scenario of Sega walking away, the probability of finding a new bidder is higher than 41%

Disclosure: I currently hold no position in GAN, Gan Ltd.

GAN Part 4B: Decision Tree Analysis (Factoring Chilean Operation Risk)

Thanks for your support!

To stay up-to-date or receive notification of when I release my latest stock pitch, please follow:

Twitter: https://twitter.com/compoundersEX

Instagram: https://www.instagram.com/compounders.ex/

YouTube: https://www.youtube.com/@continuouscompounding

Want to enjoy paid memberships for free? Help me grow by referring a friend!

1. Share Alan’s Substack: Continuous Compounding.

When you use the referral link below or the “Share” button on any post, you'll get credit for any new subscribers. Simply send the link in a text, email, or share it on social media with friends.

2. Earn benefits. When more friends use your referral link to subscribe (free or paid), you’ll receive special benefits.

Get a 1 month comp for 1 referrals

Get a 3 month comp for 5 referrals

Get a 6 month comp for 10 referrals

Update to my readers who are interested in investing in GAN. I will be factoring in risk in their Chilean operations and creating a revised part 4. It is safe to say that I am more pessimistic about this idea than I once was. Expect to see a post by tomorrow with a revised price target. My intuition is that it will be lower than $1.41 to $1.45.

If you have read my newest post on BRAG, I believe that is a better risk/reward play than GAN given that the downside is 20% and upside is 60-180%+, or a 3-6x reward/risk ratio (based on napkin math). We can size BRAG at a larger position given the lower downside and higher upside. For GAN, there is potential for major capital losses if Sega Sammy walks away and the company goes bankrupt.

I just wanted to update readers that I took profit yesterday at $1.55/$1.56.

The current trading strategy for me is to take advantage of price volatility and acquire shares if the market chooses to bring shares down to the $1.41 to $1.45 range again or lower.

If the market does this, I believe the market implied probability of the shareholder approval rate or regulatory approval rate would be too low based on my sensitivity analysis (DYODD not financial advice), which gives us a terrific risk/reward.

Also, given that this stock can go bankrupt in the worst-case scenario, please exercise adequate portfolio management and risk management. The idea with special situations like this is to be able to bet on these scenarios forever. Based on the % of your investment portfolio, think to yourself: will I be able to comfortably invest this size for the next 20 years and not risk major declines in my portfolio value? You need to be able to invest in enough of these to realize the alpha.

*Not investment advice, do your own due diligence, entertainment purposes only, seek assistance from a professional financial advisor.