SK Japan (7608) Deep Dive Part 1: Hidden Growth

SK Japan (7608) Deep Dive Part 1: Hidden Growth

*Legal Disclaimer: This post and all its contents are for informational or educational purposes only. Continuous Compounding assumes no responsibility or liability for any errors, inaccuracies, or omissions in this post, links, attachments, or any actions taken based on its contents. The information sources used are believed to be reliable, but accuracy cannot be guaranteed. Recipients of this research are advised to conduct their own independent analysis and seek professional financial advice before making any investment decisions. The opinions expressed by the publisher in this post are subject to change without notice. From time to time, I may have positions in the securities discussed in this post. The post and all its contents herein are the exclusive property of Continuous Compounding. This post is intended solely for informational purposes and is not to be distributed, reproduced, or transmitted, in whole or in part, for commercial purposes or sale without prior written consent from Continuous Compounding. Any unauthorized use, dissemination, or sale of this research is strictly prohibited and may be subject to legal action.

In this post, I go over why I believe SK Japan is value-with-a-catalyst investment.

SK Japan is undervalued given the company has been:

-increasing revenues

-has no revenue concentration risk

-has substantially untapped US revenue potential

-demonstrates operating leverage through increasing margins.

SKJ’s share price has a 50-130% upside over a 1-1.5 year holding period.

SK Japan (7608) will be releasing its financial summary of annual results on April 12th.

Post-April 12th Update: SK Japan just had a major earnings beat. Stock went up 10-15% post Q4 Financial Summary release. Paid subs who acted would be up 10-15% on the stock now (I am definitely adding to your FOMO here).

The annual report is not out yet and is to be released on May 30, 2024.

Subscribe to be the first to get my analysis of SK Japan’s annual report when it comes out!

Want to enjoy paid memberships for free?

Or…

Share my posts on Twitter:

If you repost 1 post on Twitter, I am offering a 1-month paid sub ($10 value) for free!

If you repost all 3, I’ll comp 2 months paid sub ($20 value), not bad for 10 seconds of work:

How to Navigate Japanese Filings Without Knowing Japanese Twitter Post

DM me on X after you’re done, and I’ll comp you asap.

*Those who have already claimed this offer in this post or previous posts will not be able to claim it again. Minimum threshold for followers on X is 40 to be eligible for this offer. My apologies to those with fewer followers; this is to prevent someone from creating a new account with 0 followers to abuse this promo. Offer expires at the end of May 2024. Offers may change or be removed at any time without notice.

*SK Japan reports in only Japanese. Readers should be wary of this language limitation of mine. I do not know Japanese and have used ChatGPT, Google Translate, and Google Chrome translation extensions to assist in translating Japanese text. I shall not be held responsible for incorrectly translating or misinterpreting the information sources used in this post.

Table of Contents:

-Ultra Quick Pitch Summary

-Key Highlights

-Debunking Customer Concentration

-Major US Revenue Upside (Core of Investment Thesis)

-Growth potential in Round1 JP Operations

-SK China

-Segmented Revenue Analysis

-Narrative and Hidden Advantage (Very unconcise ranting, will refine later)

Business Overview:

SK Japan has two segments:

Character Entertainment Business: This segment primarily involves the design and sale of character plush toys, keychains, and other promotional items to amusement facilities/capsule toy operators domestically and internationally, as well as planning and selling promotional products for businesses. (i.e. Round1)

Character Fancy Business: This segment primarily involves the sale of character plush toys, keychains, and other products to specialty stores and retailers, including department stores and discount stores. (i.e. Don Quijote, Pokémon Specialty Store). D2C e-commerce sales are also included in this segment.

SKJ is 32% owned by Round1, an amusement facility operator with 100 stores in Japan, 49 stores in the US, and 4 stores in China. Since 2022, Round1 has undergone massive increases in crane game machines in JP and US. Given that SK Japan supplies the prizes used in crane game machines, SK Japan is a direct beneficiary of this positive development.

My previous quick pitch on SK Japan was a quick idea going through a buyout scenario:

TLDR of the SK Japan Ultra Quick Pitch:

-Round 1 (4680) owns a 32% stake in SK Japan (7608) and is the largest shareholder of SKJ by a large margin (next in line owns 4%)

-SK Japan (706 yen per share at the time) is trading at 9.3x FY2024 P/E, 3.0x FY2024 EV/EBIT(Operating Profit). SK Japan has a market cap of 5.9bn yen and net cash of -3.3 bn yen with no debt, resulting in an EV of 2.5 bn yen.

-Given Round1 already owns 32% of SK Japan, the true price for R1 to acquire SK Japan is only 650 mm yen

-Round1 has 32.5bn yen of cash, 25.6 bn yen in debt, hence liquid net cash of 6.9bn on its balance sheet. Round1 accounts for its ownership in SKJ under the equity method (R1’s share of SKJ’s net income is recognized on the IS, and a carrying amount at cost for the investment is recorded on the BS), hence balance sheets are separate. Net cash is more than 10x over the true acquisition price and over 2x SK Japan's EV.

-Given SK Japan’s financials, R1's financials, and R1's continuous store growth trajectory, Round1 is a natural acquirer of 100% of SK Japan’s equity.

*For the initial ultra quick pitch, I initially spent very little time on the quality of the business given how statistically cheap the stock was, trading at 3x EV/EBIT, because the filings were all in Japanese. The stock looked like a no-brainer acquisition target for R1 regardless of growth prospects or revenue growth being completely tied to R1’s growth. However, upon deeper inspection, SK Japan as a standalone company has been improving it’s quality of earnings through diversified revenue growth and improving margins.

As an investor it is important to kill your original ideas once you realize the thesis has changed. I have now taken a 180 on the stock and believe it is better to long SK Japan for its growth prospects. It is better for the SK Japan investor if company is not bought out in the next 1-2 years.

Key Highlights:

-SK Japan is not as dependent on Round1 for growth as I had initially thought. Outside of Round1, SKJ generates revenue from a client base that is not highly concentrated.

-SKJ’s sales to Round1 JP increased by 71% in 2023, but Round1 sales as a % of total Character Entertainment Business remained unchanged at 29%. In fact, the entire revenue segment increased by 73% in FY2023.

-The core of my investment thesis is that Round1 has barely used SKJ as a supplier for its US operations. R1 has only started converting stores into Mega Crane Game stores in FY2024. Based on my estimate, Round1’s US Crane game machine count will increase by 3.7x by FY2025. SK USA currently accounts for only 4-7% of R1’s crane game prize COGS. If SK USA is given a COGS allocation that is in line with R1’s Japanese operations of 18-22%, we could see SK USA’s current prize COGS allocation increase 3-5x.

All-in-all, SKJ’s US revenues have the potential to increase 8-14x. This would imply a 24-39% increase in total revenue in 2 years.

-Despite R1 Japan being SKJ’s major customer, SKJ only makes up an estimated 18-22% of crane game prize COGS. SKJ could make up a larger %. If we believe SKJ can make up 25-30% of R1 Japan’s prize COGS, that would mean a 25-50% increase in R1 Japan revenue.

-Factoring the US catalyst only, SKJ’s share price has a 40-100% upside over a 1-1.5 year holding period.

-Factoring both the US and JP catalyst, SKJ’s share price has a 50-130% upside over a 1-1.5 year holding period.

Join Koyfin and save 20% using my affiliate link

My goal with any new idea is to reject it as quickly as possible. Koyfin is a huge time saver when it comes to getting up to speed quickly on a new name.

-Koyfin has one of the best screeners in the industry, with customizable formulas (create a formula to filter for net-net stocks)

-Koyfin watchlists are super intuitive, organized and easy to use

I mainly use Koyfin to quickly look at a company’s business description, valuation multiples, historical profitability, analyst estimates to gauge future prospects, and form an opinion on whether this idea is worth looking further at.

Not ready yet? Use my link for a free trial to see what you’re missing out on!

Debunking Customer Concentration:

Round1 makes up 29% of SKJ’s amusement facility sales and 21% of total sales.

For SK Japan (SKJ) to report a major customer, the customer must make up a minimum of 10% of total revenues. Since 2017, besides Round1, only Don Quijote (a retail giant in Japan known for having too many SKUs in its maze-like stores) has been reported once as a major customer in 2021. This demonstrates that SK Japan’s sales are not as concentrated as I had assumed.

Typically, the risk with having a major customer take up more than 10% of revenue is that there is a risk of the customer switching over to a competitor, and the former 10%+ revenue share drops considerably. This risk does not exist between R1 and SKJ because R1 owns 32% of SKJ. R1’s investment justification at time of purchase in late 2021, was to secure a steady supply of prizes for its crane games.

R1 may diversify suppliers in order to diversify prize offerings, but there is little to no risk of SK Japan losing substantial revenue due to R1 switching to a different supplier. R1 is incentivized to purchase from SKJ given their equity stake, which is essentially a rebate on them giving business to SKJ.

In summary, this means SK Japan has been able to grow revenues independent of Round1 with low levels of customer concentration, with no other customers accounting for more than 10% of revenues.

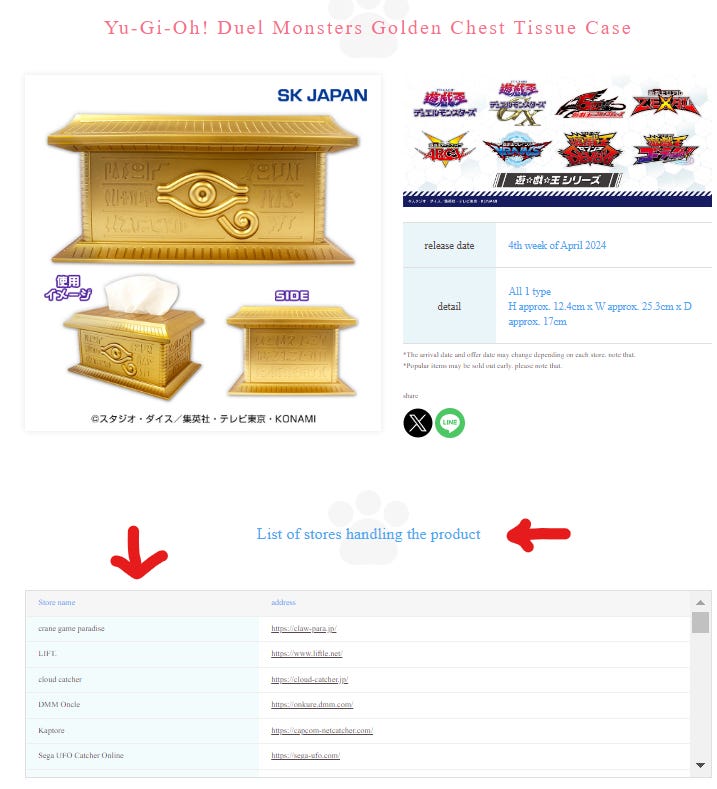

To showcase how diversified SKJ is, the following link showcases the company’s new YuGiOh Tissue box that will be releasing in late April. Simply scroll down to the list of companies selling the product.

With Excel, I counted 286 unique retail and amusement locations carrying this product. Notable companies include:

-Multiple online crane game companies

-GiGO (Genda)

-Bandai Namco

-Taito Station (Square Enix)

-Sega Sammy

-Capcom

-Other: Likely small to medium sized anime hobby stores (Manga Warehouse)

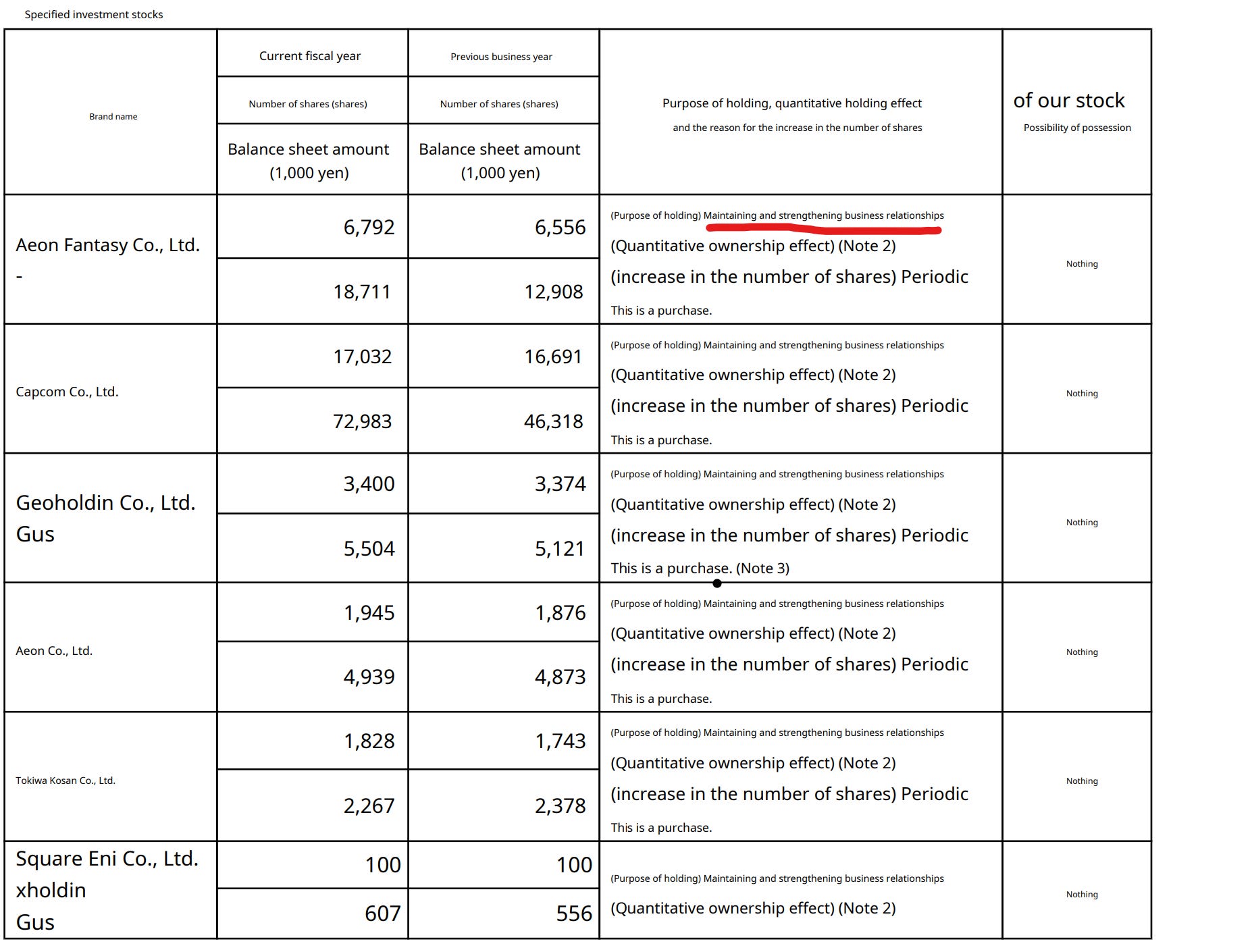

SK Japan’s clients likely also include the following:

The above are publicly traded stocks SKJ holds in its investment securities portfolio. The company states the purpose of holding the above securities is for “maintaining and strengthening business relationships.” It is funny to me that holding 100 to 300 shares can accomplish such a goal.

This disclosure tells me what companies are likely on the list of clients the company has that account for less than 10% of revenues, given that R1 takes up more than 10% of revenues and is reported.

What is interesting is that Capcom is their largest holding, followed by Aeon Fantasy. I wonder if SKJ has some insider info about those companies that we don’t have?

Track record of stock pitches:

Haier 690D: +45%

Round1: +15%

SK Japan: +15%

Okano Valve Manufacturing: +45%

GAN: +80% (closed)

CNTY: -50% (closed)

*As of May,1, 2024

Want to enjoy paid memberships for free?

Or…

Share my posts on Twitter:

If you repost 1 post on Twitter, I am offering a 1-month paid sub ($10 value) for free!

If you repost all 3, I’ll comp 2 months paid sub ($20 value), not bad for 10 seconds of work:

How to Navigate Japanese Filings Without Knowing Japanese Twitter Post

DM me on X after you’re done, and I’ll comp you asap.

*Those who have already claimed this offer in this post or previous posts will not be able to claim it again. Minimum threshold for followers on X is 40 to be eligible for this offer. My apologies to those with fewer followers; this is to prevent someone from creating a new account with 0 followers to abuse this promo. Offer expires at the end of May 2024. Offers may change or be removed at any time without notice.

Major US Revenue Upside (Core Thesis)

In SKJ’s filings, it states they do not provide a geographic revenue breakdown if domestic revenue exceeds 90%. Since SKJ has never reported in this section, it means that international revenues have never exceeded 10%.

Source: FY2023 Financial Summary

The company also noted they have 3 business entities: SK Japan Co. Ltd., SK USA Inc. and 愛斯凱杰文化伝播有限公司 (I’ll unofficially call this SK China - SKC)

Round1 (R1) underwent Giga Crane Game (GCG) conversion in FY2022. Converting stores with 80 crane games to over 300. As of the latest quarter (Q3 2024), the company has 76 GCG stores; hence, the rough estimate is 24,720 crane game machines in Japan.

In Q1-FY2024 (April 1, 2023), R1 started converting it’s US stores into Mega Crane Game stores. As of the latest quarter, R1 has 49 stores in the US and is forecast to have 52 by the end of FY2024. 37 of which are scheduled to become Mega Crane Game (MCG) stores by the end of April 2024. With the average unconverted store having 50 crane games and the average MCG store having 150 crane games, based on my calculations, the company is forecast to have roughly 6,300 crane game machines in the US by the end of FY2024.

R1 forecasts JP amusement sales to be 48.95 billion yen and US amusement sales to be 42.69 billion yen in FY2024. Despite being very close in revenue and US having only half as many stores as JP, no US revenues were reported in SKJ’s geographic breakdown section.

Why is that?

Upon looking further in SKJ’s FY2023 annual report, I found in the “Related party Transactions” (関連当事者との取引) section that Round1 Entertainment Inc. (R1’s US operations) had sales of 276 mm yen. This accounts for only 4% of SKJ’s amusement facility revenue.

Based on my estimates, SK USA makes up only 4-7% of R1’s total crane game COGS (assuming crane game revenue accounts for 25-50% of US amusement revenue).

This is consistent with geographic sales not being reported, and it indicates US and CN sales account for less than 10% of SKJ’s sales. For R1’s USA amusement sales to be 87% of JP amusement sales and yet SK USA revenues are only 276 mm yen whereas SK Japan’s sales to R1 Japan are 2,078, this indicates to me that SKJ has barely scratched the surface of its US revenue potential.

I believe SKJ’s US revenues will substantially increase for the following reasons:

Mega Crane Game Store Conversions

US new store openings

R1 USA allocating a larger % of crane game prize COGS to SKJ

Given R1 forecasts opening 10 new stores per year in the US, and I expect R1 to continue the MCG store conversions into FY2025, I estimate R1 US can have up to 9000 crane game machines by the end of FY2025. In summary, with FY2023 as the base year for crane game machine unit count, crane game machines will multiply by 2.6x by the end of FY2024 and 3.7x by the end of FY2025.

Based on my estimates, SKJ currently accounts for roughly 18-22% of R1’s JP crane game prize COGS. If we assume SK USA can account for 20% of R1’s US crane game prize COGS by FY2025, this would imply a 3-5x increase from SK USA’s current 4-7% allocation of R1’s US crane game prize COGS.

Now, a 3.7x increase in crane game machines does not imply a 3.7x increase in revenue. Increasing the number of machines simply increases the odds of a customer finding something they want to win on a single visit. i.e. Let’s assume you would play 1/100 machines. For an unconverted store with 50 machines, you may have to wait until they restock all their machines with new prizes to find the prize you want. Whereas, if there are 150 machines, you are very likely to find a prize you want to play for on your first visit. I’ll be conservative and discount the multiplier by 25%.

All in all, if we factor in the increase in crane game machines (discounted 25%) and R1 allocating a larger % of crane game prize COGS to SK USA (this should be a 1:1 conversion, unless revenues decline, which is highly unlikely), we can see a potential 8-14x increase in SK USA revenues.

In absolute terms, this would translate to 2,300-3,800 mm yen of revenue generated by SK USA alone by the end of FY2025. This would increase SKJ’s amusement facility revenues of 6,840 mm yen in FY2023 by 34-56% in 2 years all else equal. Or SKJ’s total revenues of 9731 mm yen in FY2023 would increase by 24-39% in 2 years all else equal.

Just on the impact of US operations alone, I estimate FY2025 revenues to reach 12.4 to 13.9 bn yen and operating margins to increase to 10-12%.

Based on the company’s current valuation of 10x P/E and 3.5x EV/EBIT at 757 yen per share, if multiples remain unchanged, this would imply a 40-100% increase in share price.

To simplify the complexity of comp store sales and mismatches in timing, given that there can be delays in store openings and conversions, and to factor in the scenario of Round1 USA taking longer to allocate a larger % of COGS to SK USA, I’d assume the above timeline to be between FY2025 - Q2 FY2026 (1 to 1.5 years holding period).

If we conservatively adjust our assumption to 10% of total crane game prize COGS, then simply cut all the above outcomes by half and that is still a very satisfactory outcome.

Growth Potential in Round1 JP Operations

I was trying to backout JP crane game revenues, by inversing a 60% margin profit margin on COGS.

The most bizarre thing I discovered in determining how much of Round1’s crane game COGS SKJ accounts for is that COGS is extremely small.

At first observation, COGS seems way too low at 2,356 mm yen. Given SKJ sold 2,078 mm yen to R1, that would indicate that SKJ is the supplier of 88% of R1’s COGS. And we haven’t even factored in the potential for food and beverage COGS, that would indicate SKJ is an even larger supplier R1’s prizes.

But….

Apparently, based on Shared Research’s report on R1, prize COGS are in sales promotional expenses (販売促進費)…. and not COGS.

This is a very bizarre accounting choice. The only promotional attribute of R1’s crane games is that R1 releases collaboration prizes with popular anime and artists (vocaloids, singers and idols). R1 promotes their prizes on social media, and customers will come to R1 just to win those prizes. Even if the prizes are a loss leader (which they aren't), the prizes are drawing the customers into their amusement facility, where they may contribute to the revenue of other revenue segments as well. Collaboration prizes are likely less than 10% of prizes, hence I don’t understand how they can be allocated to this category.

What makes things more complicated is that R1 does not break out marketing expense.

Based on Shared Research’s report on R1, R1 has a 60% marginal profit margin on crane games. Which is to say if it costs 1000 yen (10 x 100 yen credits) to win a prize, the cost of the prize is 400 yen. SKJ sold 2,078 mm yen of prizes to R1, which is equivalent to roughly 5,200 in amusement sales for R1 [2,078/(COGS margin= 100%-60%)].

Round1 amusement revenue was 46,940 in FY2023. If we assume crane game revenue is 50-60% of amusement revenue, then SKJ would account for 18-22% of R1’s crane game COGS. (This implies a 2-4% marketing expense margin for JP operations)

*The JP sales promotion expense serves as a sanity check, as prize COGS and marketing expense cannot exceed sales promotion expense.

*Excel Model of SK Japan will be available exclusively to Paid Subs.

There isn’t much risk in R1 giving more business to SKJ in that SKJ does not have it’s own factories and outsources all manufacturing, SKJ can certainly take up a larger % of R1’s crane game COGS. The main limiting factors are:

-The number of unique copyright licenses SKJ can obtain. Having enough diversity and volume of character prizes.

-The number of outsourced partners SKJ can attain production from

The reason R1 doesn’t give all of its business to SKJ is likely due to the owner of a certain IP deciding to design and produce the prize in-house. i.e. Sega Sammy and it’s Sonic the Hedgehog IP. Capcom and its Street Fighter IP. R1 must meet the demands of it’s customers; hence, sourcing prizes from other suppliers is a must.

As R1 USA continues to grow and expand, SKJ will be able to secure more copyright licenses and offer a larger catalogue of prizes to R1’s operations in the US and JP. I believe SKJ has the potential to increase it’s share of Round1’s JP prize COGS to 25-30% and this would imply a 25-50% increase in revenues from current levels.

If we add SKJ’s revenue growth potential onto SK USA’s revenue potential, we can expect sales to increase to 13-15.0 bn yen, operating income margins to expand to 11-13%, and assuming constant multiples of 10x P/E and 3.5x EV/EBIT, the stock price can increase in the range of 50-130% over a 1-1.5 year time frame all else equal.

SK China (愛斯凱杰文化伝播有限公司-Beijing Headquarters):

R1 currently has 4 stores in China. There is only 1 profitable store in China; hence, I will be ignoring China and their crane game machines as China is still in it’s infancy and does not need to be included in my analysis to make the investment case work, so I’ll simply treat it as a free lottery ticket if there is any growth potential in the future.

There are discussions of opening specialized crane game stores in China and to test if those can be profitable. Large stores aren’t working for SKJ in China given real estate market troubles. If the concept works, it is very good news for SKC.

From personal experience, the enforcement of IP laws is extremely relaxed in China for character IP toys and plushies. When I visited China when I was a kid, you could easily find knockoffs of YuGiOh, Pokemon, and Naruto. I doubt the situation has changed given the amount of fake sneakers and designer handbags that circulate the consumer market. Competition from illegally produced IP character merchandise is a dynamic not as commonly seen in JP or the US. As a lot of amusement facilities in shopping malls are privately owned in China, I expect margins are far better for fake plushies, than real ones, and private owners to likely opt for fake items.

The counter to this is that the Chinese middle class has grown in wealth substantially, so the willingness to collect genuine goods is an improving trend. The redeeming value of a genuine collectible is that it retains or increases in value over time if it is in good condition. Situating in more affluent cities is the approach R1 should take.

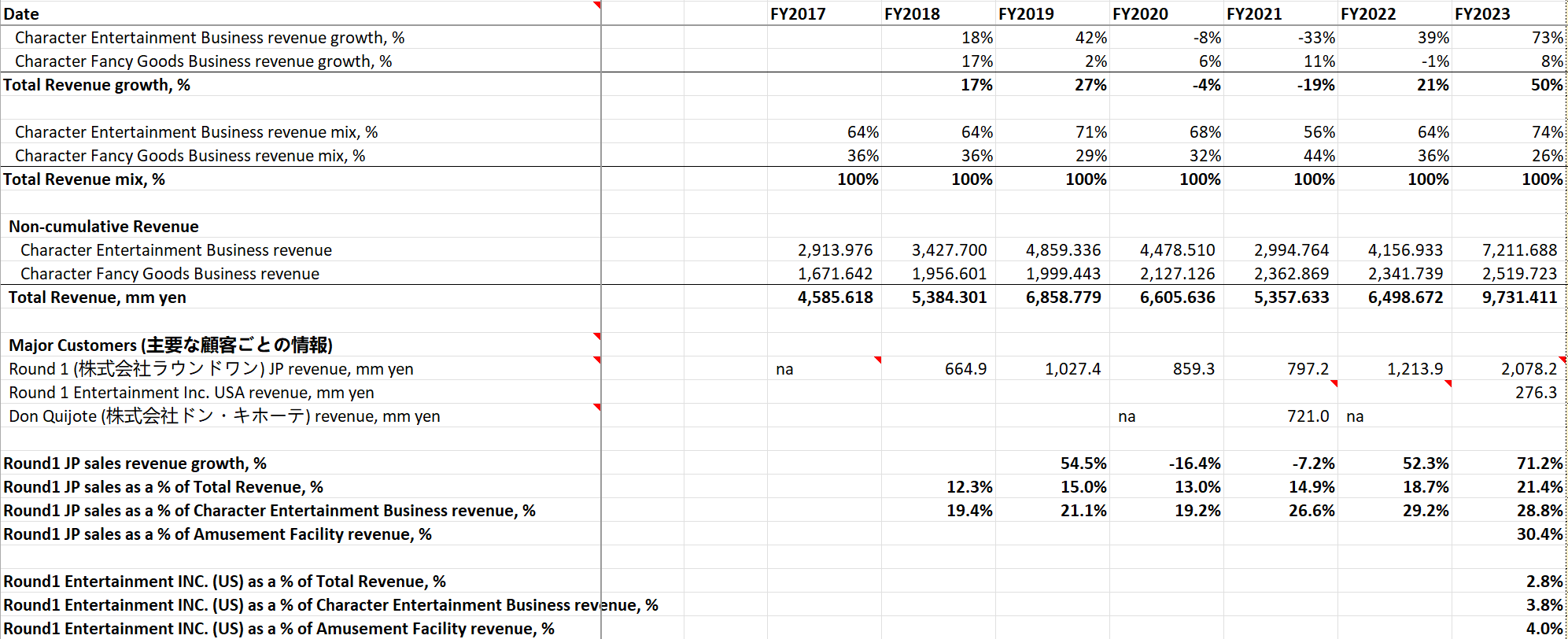

Segmented Revenue Analysis:

Cumulative Revenue Breakdown:

*This current segmented breakdown was only released in Q1-2024. The former breakdown was simply “Character Entertainment” and “Character Fancy Goods.”

Non-Cumulative Revenue Breakdown:

Character Entertainment Segment:

Amusement Facilities:

Sales to amusement facilities account for 65% of revenues in 9M FY2024, making it the largest segment of SKJ.

Cumulatively, this segment has been flat. Non-cumulatively, this segment’s performance in FY2024 has been volatile. Based on R1’s historical sales, there is seasonality in sales, and Q2 and Q4 tend to be the periods of higher sales in recent history. Q2 makes sense, as kids are on summer break during this time. For SKJ, Q2 also tends to be the best quarter in terms of revenue and profitability, but the other quarters are less predictable.

If my assumptions are correct and more sales can be sourced from Round1’s US operations, revenues in this segment could increase by 34-56% in 2 years on US impact alone.

The reason I use a 2 year time frame is that there were no Mega Crane Game stores in FY2023, we won’t have comparable store sales until a full 12 months have elapsed. As MCG store conversions are still underway, we won’t capture the full extent of Round1 US’s revenue potential until FY2025. As SKJ only reports related party transactions in its annual report and not quarterly reports, SK USA’s FY2023 sales to R1 USA of 276 mm yen are only a fraction of its future potential.

I will pay close attention to SKJ US sales to be released in its FY2024 annual report on April 12, 2024.

Capsule Toy Operators:

On a cumulative basis, sales to capsule toy operators declined 4% yoy. On a non-cumulative basis, sales declined quite drastically in Q2 and Q3 yoy.

Round1 is not a capsule toy operator; they may have a few machines at their stores, so I don’t have much insight into this industry besides my own childhood experiences. There are specialty capsule toy stores, also known as Gachapon, in Japan that have rows upon rows of capsule toy machines.

The price in Japan for a Gacha toy is 100 yen to 500 yen.

Given Gacha revenues make up only 4% of revenues, I won’t be spending much time on this. The poor performance in Q2 and Q3 could be due to lower than expected demand and/or creating an unpopular design.

Capsule toys are like the dollar store of anime goods. Those who have the purchasing power to purchase a higher-quality or larger toy would pay up at a crane game machine or go straight to a retail store. For kids, I doubt they really think deeply about the matter. Capsule toys are mainly impulsive purchases where you beg your parents for spare change. There are young adults who collect entire series of capsule toys for a series they like. The Gacha or lottery element of not knowing what figure in the series you will get is also a form of entertainment.

What is worth noting is that there are crane games where they create a big mountain of small plushies/key chains, and you can attempt to push the prizes down (Niagara Falls Method). So even in the scenario where SKJ has excess capsule toy inventory, they could sell it to R1.

Royalty Income:

I looked through the annual report and could not find any additional breakdown of royalty income. Potentially, this is royalty income generated from the company’s in-house characters.

Character Fancy Goods Business Segment (CFG):

Sales to specialty stores and mass retailers for fancy goods (SSMR):

Sales to specialty stores and mass retailers are the second largest revenue segment. This segment accounts for 30% of revenues.

On a cumulative 9M basis, SSMR grew 24%. On a non-cumulative basis, sales grew double digits in every quarter, with the largest increase occurring in Q1-2024 at 46%.

The company notes in their Q3 2024 report that this increase was due to “recovery in the number of visitors to client stores due to the easing of restrictions and inbound demand.” (translated with ChatGPT)

The company also pointed to success in the sales of popular characters like “Kirby,” "Pokémon,” and their in-house character “Faithful Dog Mochishiba.” (translated with ChatGPT)

Faithful Dog Mochishiba Official Website

What is interesting to note is that the CFG segment was able to grow revenue during COVID (FY2021).

In 2021, Don Quijote accounted for more than 10% of the company’s revenues. It is comforting to know that outside of R1’s growth, SKJ has been able to steadily increase its sales to mass retailers and specialty stores.

I have not done extensive research on SKJ’s customers in this segment but potential tailwinds would be:

-SKJ’s customers opening new stores

-SKJ’s customers allocating more shelf space for IP character merchandise.

-Overall increase in demand for anime products

E-commerce:

Link: SK Japan E-commerce Website

E-commerce only accounts for 2% of sales.

E-commerce is still in its infancy, hence why the revenue growth percentages look so impressive.

The most recent Q3 quarter was one of their best quarters, but the company did not comment on the e-commerce results in their latest Q3 report.

After browsing their e-commerce website, I found it to be a very standard e-commerce website, nothing special. It simply provides another channel to attain SK Japan products. D2C margins are likely better for SKJ as well. In addition, SK Japan isn’t restricted on price of the goods it can sell on its website, whereas there is a government limit on the value of typical crane game prize where the prize’s retail value cannot exceed 1000 yen. I personally don’t think companies really follow this rule or that it isn’t enforced, given that there are games that cost 500 yen per attempt.

I will say, I don’t see some popular prizes in their crane game segment on their e-commerce site. This could be because they are sold out or some products are exclusively sold to amusement facility operators.

Narrative and Hidden Advantage:

The company states that 50% of the market for prize products is 50% owned by the major gaming machine manufacturers. i.e. Sega Sammy, Capcom, Square Enix (Taito Station) and more. The rest is split among 30 other companies, including SKJ.

Current Bear Narrative:

-SKJ competes in the other 50% highly competitive industry

-The company lacks any valuable in-house IP, besides Mochishiba, and has to acquire character IP from licensors. SKJ is effectively at the mercy of IP holders.

-The company has no competitive moat.

-The only thing making SKJ slightly better than the other 29 competitors, is that they are 32% owned by Round1 which is a large customer

Hidden Bull Narrative:

In undergrad econ we learned about what happens if there are profits that exist in a perfectly competitive market. There will be new entrants entering the market until profits go to zero, then some participants will go bankrupt and profits go back up again, and the cycle continues.

On the surface, this is the landscape that SKJ likely competes in.

But not entirely:

We also learned that in order to not have to compete in a perfectly competitive market, one has to make differentiated goods.

How is SK Japan differentiated?

There are 3 main areas the remaining 50% of the market can compete on:

Brand reputation

Longevity and consistency

Quality of product produced

General Quality

Meeting safety protocols and the safety of children

Design

Volume

-Brand Reputation: Something I haven’t quite gotten any conviction on is SK Japan as a brand. Maybe a reader who is from Japan can shed some light. As I didn’t grow up in Japan, I am not sure how consumers view SK Japan. Upon inspecting Ebay, it seems SK Japan plushies and collectibles do go for premiums on the resale market. This points to some level of collectability, reputation, and quality in the consumers mind. In my opinion, everything from the character design to the product presentation and packaging are consistent with a well-established brand.

Also, I couldn’t find any controversies, product recalls, or products that hurt children from SK Japan. This is an often overlooked aspect of ensuring toys are safe and meet safety standards in the design phase.

-Longevity and Maintaining Business Relationships: The company has been servicing the amusement crane game prize industry for over 30 years. The founder, Toshishi Kubo, was a successful salesman before quitting his job and founding SK Japan in 1989.

In the early days, Kubo visited every single business he supplied to build relationships. They have established years of relationships with nearly every possible amusement facility company on the market. The company apparently has strict training on how new hires greet clients and how they present themselves. In Japan, a lot of business still value in-person visits as a form of respect and to show you value their business relationship. One would think that once Round1 acquires 32% of SK Japan, there would be burned bridges. Having inspected the locations where character prizes are available, SK Japan continues to supply to all the big names with no broken bridges that I can see. This signifies they have maintained a healthy business relationship with their clients.

-Design: Once SK Japan acquires a license, it is up to them to design the character merchandise. The licensor simply approves of the design to ensure quality is up to their standard and consistency with their brand image. The company has 128 employees and the average tenure at SK Japan is 10.2 years (as of Feb 2024). If this is representative of the tenure of those on the design team this is good news because we can expect a seasoned design team designing products for SKJ.

Anecdotally, I was looking at their YuGiOh products and I did find that their products are a true representation of the IP brand. They did not butcher any designs. I can see myself genuinely wanting their products if I was a kid. Even right now, I want their YuGiOh tissue box on my coffee table because I know my friends will be pleasantly surprised when they see it and it’s a talking point.

-Volume: The biggest competitive advantage SK Japan has over the other 29 competitors that aren’t the big amusement machine manufacturers is order quantity

When a business makes an order with a factory, there is something called a MOQ (minimum order quantity). For the factory to fill an order, a business must place a minimum order of a certain quantity. Typically, the more you order, the better your margins will be. This is due to certain fixed costs the factory must overcome for the business transaction to make economic sense for the factory. Quantities well in excess of the MOQ mean better margins for the factory because fixed costs are fixed and fixed cost per unit of product drop the more you produce. The factory wants to incentivize large orders; hence, it will pass along some of the cost savings to the buyer by offering a cost per unit for the buyer at different quantity thresholds.

Here is a video showcasing the process of how a plushie is made in a factory in China:

In the video, they pile 10 sheets of fabric over each other (I guesstimate 1.5 meters by 7 meters for each sheet). They then fold the fabric and transport it to a press cutter (20 layers once folded). They then take a pre-molded steel stencil cutter and place it over the layers of fabric. A factory worker then presses the buttons on a pressing machine to cut the fabric with the stencil cutter. From what is shown, the most efficient order volume is one that fills up the entire 10 sheets of fabric. It takes the same amount of time to create the stencil cutter if you use it to cut fabric for 500 dolls or 1000 dolls. Given each punch from the cutter is 20 sheets of fabric, this factory likely has a large MOQ for plushies.

This is simply one factory and potentially this factory is one you would go to for larger orders. There are possibly smaller factories who are willing to do smaller order quantities.

Given SKJ does not have it’s own factories and outsources production to domestic and international manufacturers, SKJ’s margins are a function of mainly:

1) the cost of the IP copyright license

2) Getting the cost per unit as low as possible. Or, in other words, the higher the order quantity, the better.

1- Typically, license agreement stipulate a fixed fee or revenue share. For a fixed fee agreement, SKJ has to be confident in its forecast of demand. If the economic reality is that demand is higher than what the cost of the IP license implies, then SKJ margins increase by the discrepancy. On the contrary, SKJ’s margins dwindle if they overpay for a license and demand is not what they had expected. This can be avoided by a revenue share agreement where a % of revenues, no matter the quantity, goes to the licensor. I believe a fixed fee agreement has the potential for much larger margins if you believe demand is far greater than what the licensor thinks the demand is because the fixed fee per unit drops as you produce more. Revenue share is likely a safer bet for both licensor and licensee who don’t have conviction of what demand is. I have no insight on what type of agreements SKJ gets into.

2- This is where SKJ’s hidden in plain sight advantage lies - Round 1. On the surface, one may think R1 has a significant influence on SKJ and may give itself preferential terms. To some extent, it has influence, but Round1 is effectively a customer that meets a MOQ for every order.

I see this purchasing power as a competitive advantage, but not quite as strong as a competitive moat. A new entrant trying to copy the SKJ business model can’t just sign up a repeat behemoth customer like Round1. SKJ has over 30+ years of experience. There is some value in it’s longevity and consistency. SKJ lacks A- or S- tier in-house character IPs that gaming and anime companies have, hence why I believe they don’t have a moat, they are in some ways at the mercy of copyright license holders. The competitive advantage they do have is a purchasing advantage that certainly helps with margins.

R1 making up 29% of amusement facility sales may seem like poor concentration, but it is in all actuality a blessing in disguise.

Let me explain. Let’s say you run a bakery that specializes in cookies. Across the street from you is a luxury condo where Roger, the CEO/owner of a utility company, lives. Roger is a cookie fanatic, and he absolutely loves your cookies. He becomes addicted and decides that his office should have cookies all year-round for him and his employees to enjoy. So the CEO tells you that he wants 300 cookies sent to his office every day, but he has a catch. You are excited because that is 33-50% of your current daily output. Given how much predictable business he is going to give you, he wants to invest in your business. He wants to purchase 32% of the business at a fair valuation. You agree because you want to open a second bakery and expand.

Let’s analyze this scenario and what this has done for your bakery:

-You have now secured a stable minimum daily order quantity

-Your daily sales are now more stable and less volatile.

-Due to this massive order, your daily output goes from 600-900 to 900-1200. Your margins have thus increased due to economies of scale. You can bulk buy more flour, sugar, and other ingredients.

-The CEO is unlikely to direct business to any other bakery given his own personal equity stake

-The CEO is busy with making mills and bills from his utility business that he is unlikely to compete with or acquire you.

Going back to SKJ, when SKJ designs a new plushie, they know Round1 is good for a certain minimum order. Round1 is a stable and returning customer. SKJ can now increase it’s order size and improve it’s margins. To make matters even better, Round1 has an entire US operation that has barely made any orders. This is equivalent to the CEO telling you he is adding another power plant and he’ll need another 300 cookies for the employees there.

Hence, Round1 is a client of SKJ who’s minimum order quantity per design is ever increasing as new stores are opened. Given this order quantity cost advantage, SKJ is likely the last company to go bankrupt, even if it operates in a competitive market. Furthermore, they have no debt and 2/3 their market cap in cash. SKJ has the capital to weather any storm.

I will make the weak argument that SKJ’s products are differentiated due to brand reputation, longevity, quality, collectability, and design. And make the strong argument that SKJ’s order quantity advantage is what will allow it to outcompete it’s comparable competitors that have a similar business model.

Now your counter to my claim could be that SKJ is only a 6bn market cap (40mm US) company; any company with a larger market cap could easily exceed it’s purchasing power.

Now my reply to you is that it is great that SKJ competes in the hype-driven and trend-following market of crane game prizes. Inventory ideally isn’t sitting for a year or even more than 3 months if I were to guess. Amusement operators want to get rid of their prizes in days, weeks, or a few months. You can have the same purchasing power as SKJ, but do you have the DISTRIBUTION?

A competitor that has capital and purchasing power, but no one to sell to can’t compete with SKJ.

My point is proven in that Sega Sammy (420 bn yen MCap), Capcom (1.1 trillion yen MCap), and Genda (100 bn MCap) are all customers of SKJ.

Now the last piece of the puzzle. All these numbers, assumptions, and theories are nonsense if the customer doesn’t want the prize.

Let’s visualize for a second: you operate one of Round1’s Giga Crane Game stores (300 crane game machines) and you are in charge of inventory management. Your pay is directly tied to reducing inventory costs, generating revenue, and maximizing profits. You look down at a supplier’s list of 40 prize suppliers. 10 are the major suppliers, and 30 are far smaller.

Your first decision point is whether you want to run a concentrated strategy or a diversified strategy.

You decide to follow a concentrated strategy. You focus on the top 10 major suppliers with the best IPs. You run this for 1 month and find that the sales on 200 (66%) of the machines are great, but the other 100 aren’t doing so well. This is likely due to an overlap of the same types of prizes from the same companies within the same store, across the street, and in the area.

While surveying the game floor, you overhear one of your crane game staff being asked by a customer whether there are prizes for a certain anime. You reach an epiphany and ask your store staff to take note of whenever a customer requests a certain anime prize. At the end of the month, you have compiled the list of requests and rank ordered them from most requested to least. You also do some market research on the popular anime titles being released this season.

For the next month, you decide to try out a diversified approach. 200 of the crane machines are allocated to the top 10 suppliers. The remainder 100 are for less popular, requested, and even niche anime sourced from the remainder 30 suppliers. Sales increase, but you notice a new phenomenon. Out of the 200 crane machines that did well with the 10 largest suppliers last month. 50 of them did poorly this month. You see a kid playing for the prize of the same anime on a different machine with a different prize. You ask the kid why aren’t you playing on this machine instead. The kid responds, “The design is ugly.” You ask several customers the same question, and the response varies in that the prize is ugly, does not look like the anime character, or the character is no longer popular because another character defeated it in battle. You come to the realization that there is concentration risk in offering purely what is popular.

The next month, you lower your order volume in favour of lower concentration risk. This lowers inventory costs because if a prize is unpopular and doesn’t sell, you can immediately switch it for something else likely to sell and not have it take up precious crane game window space. If a prize is doing well and sells out, you can order more.

You come to the realization that it is better to earn a smaller margin on a prize that generates revenues than a larger margin on a prize that doesn’t sell. This is likely the market dynamic that exists and why SKJ can compete and earn operating margins in the low teens—very uncharacteristic of a perfectly competitive market condition where SKJ is undifferentiated, right?

Ways to win in this investment:

-Positive carry with div. yield (interim 10 yen div. per share, 2 dividends per year, 3% div yield approx.) exceeding margin on IBKR (hence you don’t need to take FX risk)

-Buyout by R1 (some premium)

-Growth (anime tailwind, R1 US store expansion and conversion tailwind, higher COGS allocation tailwind in JP and US)

-Market realizing US revenue is mostly untapped

-Analyst coverage, currently 0

-I will email the company about corporate governance soon…. (as per the instructions of AltayCap)

-Share buyback (excessive amounts of cash)

This was a long post and part 2: Qualitative Analysis will be released soon.

Disclaimer: I am long shares of SK Japan (7608) at the time of publishing this post.

To stay up-to-date or receive notification of when I release my latest stock pitch, please follow:

Substack:

Twitter: https://twitter.com/compoundersEX

YouTube: https://www.youtube.com/@continuouscompounding

Instagram: https://www.instagram.com/compounders.ex/

r/TSEvaluestocks: https://www.reddit.com/r/TSEvaluestocks/